See more episodes of Quant Concepts here

Ian Tam: Welcome to Quant Concepts. With three quarters of the year behind us, 2019 has shown to be an exceptional year in the domestic equity markets with the TSX Composite showing impressive total returns exceeding 20% year-to-date. For those that continue to be cautiously optimistic. This week, I'll use Morningstar CPMS to look for small and mid-cap names outside of the TSX Composite Index.

Recall that typically in volatile markets small-cap companies tend to move more quickly than their large-cap counterparts. This week's strategy aims to temper this expected volatility by looking for the traditional defensive characteristics of dividend growers within that small and mid-cap space in Canada.

So, having a look at my Morningstar CPMS screen here, I'm going to build this model by first taking all 710 companies that we track in Canada and ranking them based on three very specific characteristics. The first characteristic is going to be the yield on expected dividends. So that's the yield based on what the company has announced they're going to pay but have not yet paid. I'm also going to look at the standard deviation of total returns over the last 180 days against, standard deviations, measures basically how consistent something is. So, a company whose stock price moves very quickly or rapidly up and down will have a very high standard deviation of returns. And what we prefer is a company with a lower standard deviation of returns or a more consistent return pattern over time. And finally, to make sure the companies can pay dividends over time, we're looking for companies with growing cash flows. And here we're looking at the five-year growth rate of operating cash flows for the small-cap, equity space. So, we're going to take that 700 companies that we track in Canada, we're going to sort them based on those three factors as our first step in our strategy today.

In our second step, we're going to take a look at the top 35%, roughly the top third of that universe, and the first thing we'll do is screen out any of those names that happen to be in the TSX Composite Index. And today that's about 240 names, we're going to take all those names out to really just focus on that small-cap and mid-cap space in Canada. We're also looking for companies that pay a dividend greater than zero. So basically, any dividend works for us today, we're looking for a positive five-year cash flow growth rate. And then we're also looking for a reasonable payout ratio. So, in the past, I've mentioned payout ratio as a way to measure how sustainable a company's dividends are in the past, and hopefully in the future, as well. So, we don't want a company paying out too much of their earnings or too much of their cash flows in the form of dividends, that is not sustainable in the future.

So, specifically in our model, today, I'm going to look for a payout ratio on earnings that's less than 80%. Any payout ratio on cash flows, that's less than 60%. We're also going to look for companies that have a three-month price change in a positive direction. So, basically, we want to make sure the momentum is in the correct direction before we purchase the stock. And finally, we also want to make sure that the market float is greater than about $110 million. So, we are looking for that small and mid-cap space. But we certainly don't want to be caught in any liquidity issues by investing in particularly small and micro-cap companies. So, we put a lower limit on this, we've also put an upper limit on the market float of about $1.5 billion, just to make sure if a company doesn't happen to be in the TSX Composite Index, but it's a bit larger. We don't want to put that in our model today, because we are focused on that mid-cap, small-cap space.

So those are my buy rules. And my final step in building this model is to define my sell discipline. And what we're going to say here is if the stocks rank, which is based on the three factors in my pie chart, if that rank drops below the top 35%, I'm going to sell the stock, as well as if the company's payout ratio goes beyond 90% on earnings or 80% on cash flows, respectively, I'm going to sell the stock. And finally, if the company happens to cut its dividends in a given quarter, I'm going to sell that stock right away.

So that's my model today, and I'll use Morningstar CPMS to backtest this to see how it would have done over a very long period of time. So, I'm starting my backtests in January of 2000. So, this is just before the tech bubble. And we're starting with a portfolio of 15 stocks that met my requirements using the information from that point in time. At the end of each subsequent month, if any of those stocks, break my sell rules, I will sell the stock and immediately replace it with the next highest-ranking stock in that same month, never owning more than four stocks per sector.

Now because we are in that mid-cap, small-cap space, I did bake in liquidity costs. So that means every time I buy and sell stock, I'm buying the stock for 1% higher than the close price, and I'm selling the stock for 1% lower, because just to account for the small-cap nature of this strategy and the fact that some of these stocks aren't going to be as liquid. The second thing I wanted to also note on the back-test today is that I'm going to use a slightly different benchmark because we're outside of the index, I decided to use the TSX SmallCap Total Return Index as more of a fair comparison against my strategy.

So, having a look at the back-test results here, you can see the strategy return an annualized total return of about 11.5%. That's net about 1% liquidity costs I talked about, compared against the TSX Small Cap Total Return Index, that's about 7.7% better on an annualized basis. So certainly, quite a better performing strategy than the index. The turnover on the model is about 34%. So, on average, we're trading about one third or about five stocks in and of the model every single year. More importantly, the point of this model was to look for more of a defensive characteristic strategy. And one way to measure that is to look at how the strategy would have performed when the index was down. So, if you look at all the quarters over the last 20 years or so, where the small-cap index showed a negative return, this strategy beat that index about 91% of the time. So very defensive in nature especially when compared to a small-cap index.

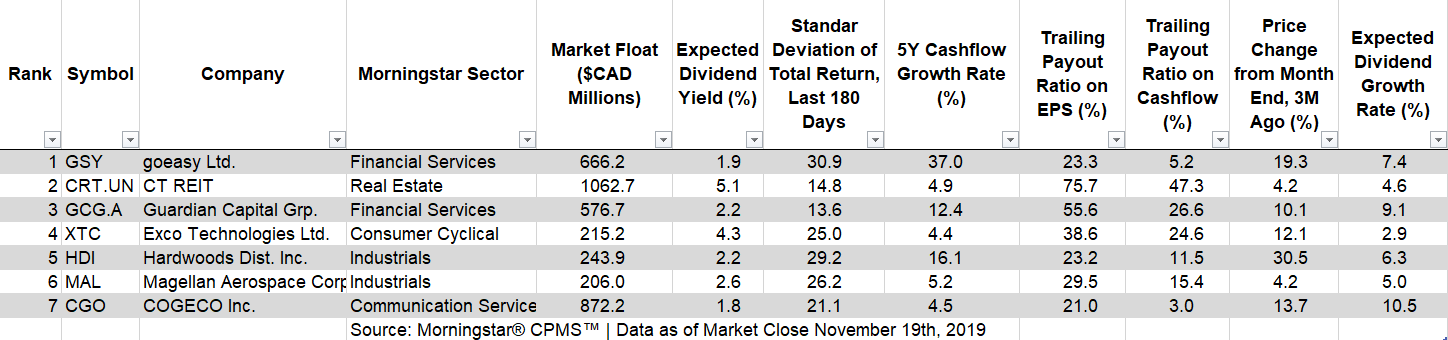

The second thing I also want to outline is our Sharpe ratio. So again, the Sharpe ratio is your risk-adjusted return or another way to say it is how much return are you getting per unit of risk that you're taking on. So today, our strategy over that 20-year time frame showed a Sharpe ratio of 0.8 compared against the index, which has actually had a very low Sharpe ratio of about 0.1. So certainly, more of a risk efficient strategy than simply buying the small-cap index. So, the stocks that meet the requirements to be purchased into the mall today are listed in the table accompanying this transcript.

For Morningstar, I'm Ian Tam.