See more episodes of Quant Concepts here

Ian Tam: Welcome to Quant Concepts. Value investing traditionally involves buying companies at a discount to either their fair value price or they're trading at valuation multiples that are lower than their peers or the market itself. The idea of value investing does make a lot of sense. And studies have shown that over multiple decades, value messaging does seem to pay off. But over the last number of years, value-oriented investors in Canada have had a really tough ride with the style itself generally underperforming other styles as well as the market on whole. All this said, the market does have the tendency to mean revert. So, if you are of the belief that value-focused investing might come back in favour, today's model might offer you some reasonable ideas. So, I'm going to use Morningstar CPMS to build the model that does focus on value, but on a relative basis, with an additional focus on quality over a very long period of time.

So, having a look at my screen here, you'll see I have a very traditional pie chart that outlines the metrics or factors I'm going to use to first rank a number of stocks. Today's universe is going to be the S&P/TSX Composite, which consists of roughly 230 companies. And in my first step of building a quantitative equity model, I going to take those 233 companies and sort them based on two factors. The larger factor here, which is where 75% of my model, is the deviation around 10-year earnings per share. So, basically, we're measuring how consistent a company's earnings have been over the last 10 years. And of course, we want more consistent companies. Those will be ranked a little better in my model. I also am going to look at another quality metric which is return on equity. I'm just going to look at the return equity on average over, again, the last 10 years. So, two fairly long-term measures of quality and those two factors are going to be used to rank the stocks in the S&P/TSX Composite.

So, so far, I haven't actually used any value factors in my model. But in my second step, what I'm going to do is then screen out based on a number of relative value metrics. So, to start with, I'm going to look at the top quartile of stocks based on those quality metrics. Within that top quartile or top 25%, I'm going to screen out companies that are trading above their sector median valuation metrics. And today, I'll actually use four different valuation metrics or valuation multiples.

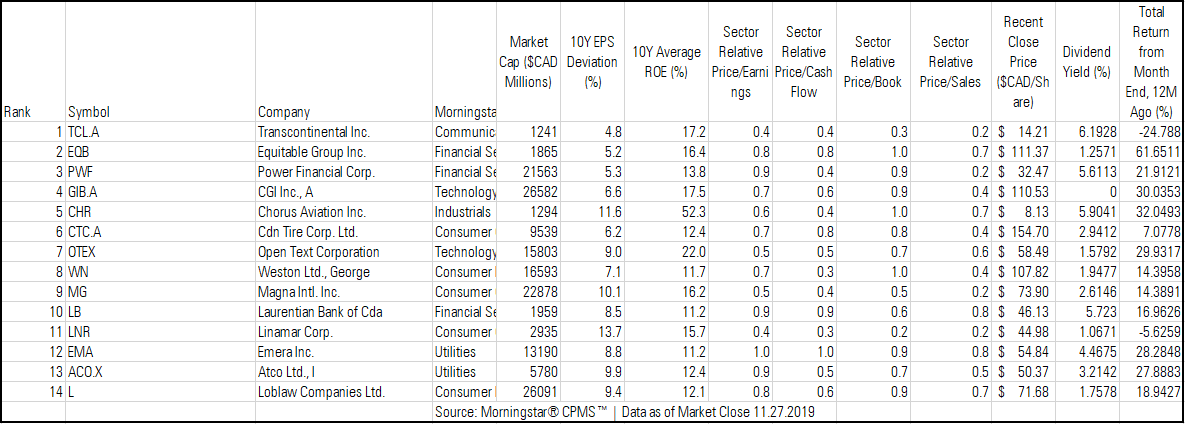

The first one I'm going to use is price to earnings, so a P/E ratio. I'm also going to use price to cash flow, price to book, as well as price to sales. So, today, I'm not using the straight price to earnings or price to cash flow metric. I'm taking the price to earnings metric, for example, and comparing it against the median price to earnings of the sector to which that stock belongs. So, in the table that's going to be accompanying today's article, or video, what you're going to see is a number of numbers ranging from 0.2 to 1. If you see a 0.9 in the table, what it means is that company is trading at 10% lower in terms of its valuation than the sector to which it belongs.

So, again, what I'm doing here is making sure that all the stocks that meet my requirements are actually trading below all four of these valuation metrics relative to the sector median. So, those are my buy rules.

And of course, when we build a quantitative equity model, we also want to define a sell discipline. And what I'm going to do today is, if the stock drops below the top 35% in terms of its rank, we sell the stock. Or if the company exceeds 50% above the sector median valuation ratio, I will also sell that stock. So, basically, if the stock becomes overvalued, I'm going to remove that position from my portfolio and replace it with something else. So, those are the value-focused metrics I'm going to use today. And again, if you believe that value will come back in style, this strategy today might offer some reasonable ideas.

So, to test the validity of this strategy, of course, we're going to back test this over a very long period of time using Morningstar CPMS. So, today, I'm going to start my back test back in December of 1995. That's, of course, before the tech bubble as well as before the financial crisis. Starting with a portfolio of 15 stocks, with no more than four stocks per sector. In December of '95, I would have purchased whatever 15 stocks met my requirements using the information available from that point in time. Today, I'll start with $100,000 portfolio, again back in December of 1995.

I'm also going to bake in a $25 transaction cost today. So, for every time I trade a stock, I'm paying $25 out of my own pocket, just to account for a real-life scenario where that actually happens. Just as the back test is finishing up here, you'll notice that my statement at the beginning of the video does make sense over a very long period of time – value investing does tend to produce reasonable results. Now that the back test is finished, we'll talk about the overall results for that period of time.

So, the return on the portfolio ended up being roughly 12.2% annualized. That's better than the S&P/TSX Composite by roughly 4.3%. So, certainly, not a bad model over the longest timeframe. Just looking a little closer though at the trailing returns, you'll notice that on a one-year trailing basis, or 12-month trailing basis, the strategy was actually fairly close to the index. So, slightly underperforming the S&P/TSX Composite. If you look at over a three-year, over a five-year period, you'll see that again, we're either slightly under or close to the index. So, again, the idea of value investing has certainly underperformed over the last, in this case, five years. But if you look at over a much longer timeframe, it does tend to produce reasonable results. So, when the investors favour growth over value or value over growth, when that trend changes, it's not obvious to anybody. But if you believe that that trend is going to change soon, perhaps this might be reasonable to look at a bit more closely.

And of course, usually, when we create these models, we also want to look at the risk metrics. So, if I scroll down a little bit of my screen here, you'll see that in all the quarters where the TSX was down, my strategy beat the index about 70% of the time. So, again, fairly defensive, which is no surprise because we use a couple of fairly long-term quality metrics to rank the stocks to begin with.

Also, we want to look at the Sharpe Ratio. That's your risk-adjusted return or the amount of return you're getting per unit of risk that you're taking on. Our Sharpe Ratio over the longest timeframe is about 0.7, with the index being about 0.4. So, of course, we want a nice high Sharpe Ratio, which certainly, this is reasonable in my model today. So, the stocks that meet the requirements to be purchased into the model today will be listed in the table attached to the transcript to this article.

For Morningstar, I'm Ian Tam.