Being a well-informed investor is both a blessing and a curse. Fears of the economic impact of the COVID19 have dominated news feeds, markets have been more volatile than usual, and on Tuesday morning, the U.S. Fed cut rates by 50bps in an emergency move to protect the US economy from the fallout of the virus.

It takes an immense amount of discipline to not be shaken, or at the very least deeply concerned about the state of the world economy and how this impacts your investment portfolio. It’s times like these that take an emotional toll that might prompt us de-rail our own investment plans. Here are some key points that might help stay the course:

1. Risk is relative: Short term market volatility should not affect how much risk you take on. If you feel like the change of your portfolio value over the last few days is too much to handle, you are probably taking on too much risk. Use this attention and energy to reconsider your risk budget and act accordingly to ensure that your long-term asset allocation (the mix between stocks, bonds, cash, and other asset classes) is right for you. Remember that the closer you are to retirement, the less risk you can afford to take.

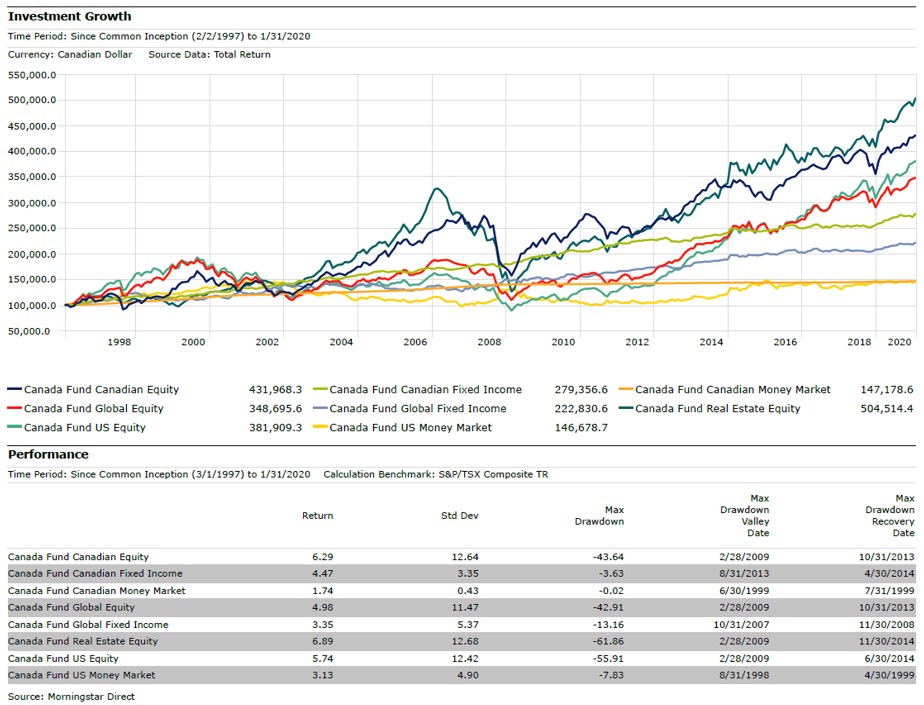

Here’s a reminder of a ‘worst case’ scenario illustrated best by the systematic financial market crash of 2008:

This shows the long-term performance of several popular Canadian fund category averages, coupled with a table that shows the max drawdown of each category. Max drawdown measures the portfolio value drop from the highest peak to the lowest subsequent valley in an investment. For most fund categories, this happened during the financial crisis.

The max drawdown recovery date indicates when the original peak portfolio value was recovered. For riskier categories like Canadian or global equities, the recovery period was about five years. If you had been invested purely in equities and planned to retire during the financial crisis, it was likely that you would not have been able to do so. This is the ultimate failure of a financial plan. On the other hand, if you had been invested purely in Canadian or Global fixed income, the impact of the market drop would have had a negligible impact on your ability to retire during that same timeframe. A mix of multiple asset classes with low correlations to one another will help you be invested according to your risk tolerance.

2. Don’t time the market. The most sophisticated investors in the world cannot predict what will happen tomorrow, and neither can we as retail investors. By nature, the farther out financial models forecast into the future, the less accurate they are. Take these forecasts with a grain of salt. We’ve just wrapped up the 2019 RRSP contribution deadline here in Canada, so many Canadians might be considering ‘holding back’ in terms of investing. Remind yourself that dollar-cost averaging does not afford you more wealth in the future and investing according to your long-term asset allocation is the best plan to ensure you reach your financial goals.

For investors that have these two concepts in check, staying the course and allowing the effects of diversification and compounding to do the heavy lifting will likely lead to a successful path to financial independence.