On April 20, U.S. oil prices dipped into negative territory and Brent crude swooned shortly after. The coronavirus has wreaked havoc on worldwide consumption of gasoline and other crude products, and the supply response thus far has been lethargic and ineffective. As a result, storage utilization is dangerously high, and investors who paid heavily to escape short-term crude futures may yet breathe a sigh of relief. Even before the latest oil collapse, the outlook was bleak: The 9 million barrel/day decrease in global demand that we now forecast due to COVID-19 eclipses prior downturns, and brinksmanship by Russia and Saudi Arabia has delayed a crucial response on the supply side.

But extrapolating Armageddon oil prices to infinity is a mistake. We think the GDP impact of COVID-19 will be modest in the long run. Once a vaccine is developed, we see little reason for demand for most oil-related items (even for air travel) not to fully return to normal. If the intensity of consumption is not severely affected, we will eventually see strong catch-up demand, which cannot be satisfied without a contribution from U.S. shale--and that business model simply does not work at strip prices. The marginal cost for shale producers is US$55/barrel (West Texas Intermediate), and without a recovery to that level, shale investment will fall far short of what’s necessary.

Storage fears send crude tumbling

WTI crude spiraled into negative territory on April 20 as oil traders played a high-stakes game of musical chairs. Widespread social distancing due to the coronavirus has dragged down oil consumption, and storage utilization at the Cushing hub, where delivery of the WTI contract occurs, is rapidly climbing. Storage utilization has been sharply rising for the United States overall in recent weeks, due chiefly to the dearth of oil demand because of COVID-19. However, utilization in Cushing has surged the most, going from 50% in early March to 72% by April 10. If this rate of increase continues, Cushing’s tanks will be full by mid-May. Practical limits could be reached much earlier than that, given that utilization never rose above 90% in the prior oil downturn in 2016.

That makes front-month futures contracts much riskier than usual--nobody wants to take physical delivery if there’s nowhere to store it. In the April 20 scramble, some investors paid as much as US$40 per barrel to offload futures for May delivery because if Cushing does get full, it could cost even more to find an alternative home for physical barrels at the time of delivery.

The significance of the declines was probably overblown by intense media coverage, given that longer-dated futures were affected much less severely. In our view, any physical constraints will evaporate once OPEC cuts kick in and COVID-19 isolation ends. So, it doesn’t make sense to discount long-term prices for storage risk.

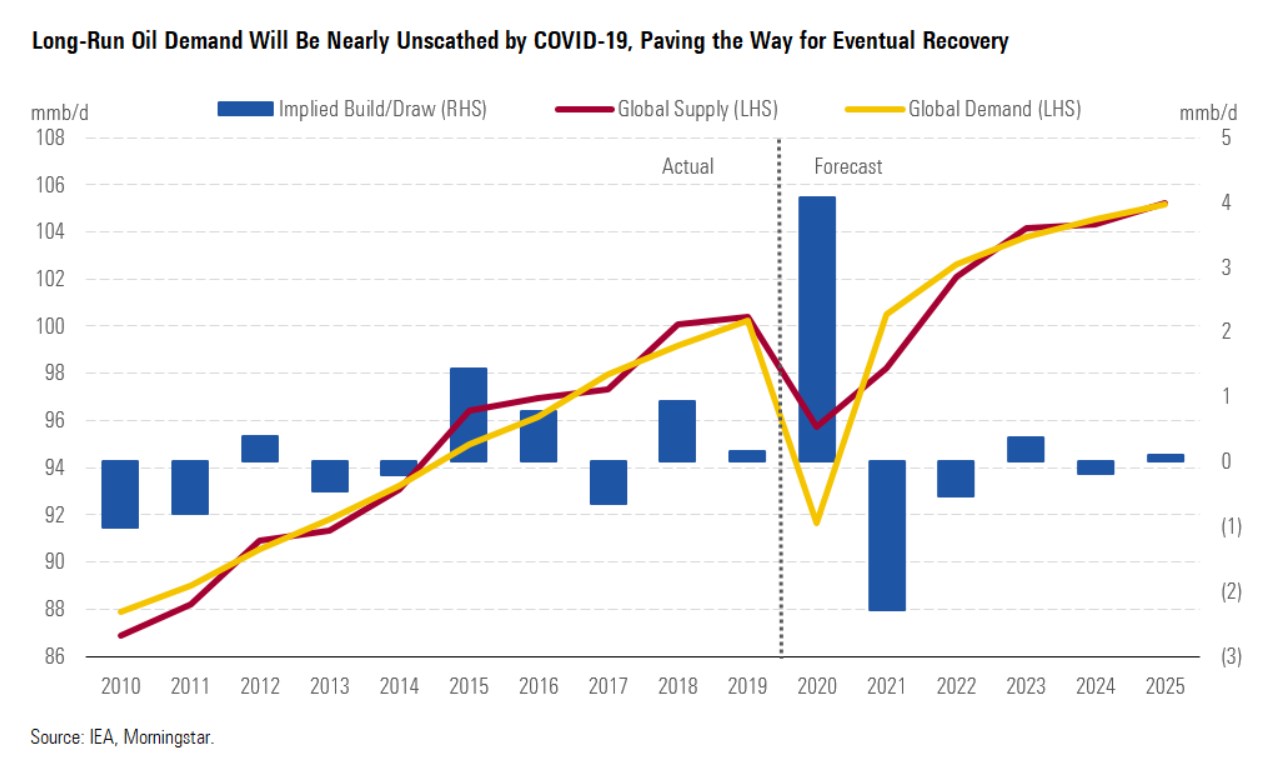

2020 set for historic demand decline, but with a quick bounce back

We now expect a 10 million barrels per day impact from COVID-19 on global oil demand in 2020. Subtracting this impact from our pre-COVID forecast (about 1.2 million barrels per day growth) yields our new forecast for an almost 9 million barrels per day (9%) oil demand decline in 2020.

This is a stunning hit to demand by historical standards, easily surpassing the 1.6% decline in the prior recession (2007-09). No one-year decline in oil demand in the post-WWII era comes close, although we did see a 10% cumulative demand decline from 1979 to 1983 in response to the oil price shock of the late 1970s. While this forecast might seem sensationally bearish, we think it’s very much realistic (and roughly in line with leading-edge consensus--the International Energy Agency’s newly released April oil market report projects a 9.3 million barrels per day demand decline in 2020).

Our oil demand forecasts draw on Morningstar's macroeconomic work, which incorporates the impact of COVID-19. We forecast a 1.4% fall in global real GDP in 2020, incorporating a 460-basis-point impact from COVID-19 (compared with our pre-COVID-19 expectation of 3.2%). However, we still don’t think it’s time for investors to panic on oil demand. Crucially, we believe that oil demand will see dramatic catch-up growth in 2021 and afterward.

We expect jet fuel and gasoline (8% and 26% of global oil demand, respectively) to drive over 70% of the hit to 2020 oil demand. Our forecasts are informed by our month-by-month projections for COVID-19 outbreak severity in the U.S. and implementation of mitigation measures including business closures and voluntary social distancing. In our base case, we expect the need for social distancing to fall dramatically in the second half of 2020, as we project a much lower fatality rate thanks to the development of effective drug treatments. While we developed this model for the U.S., it is a good guide for what to expect for the rest of the world on average.

We don’t think demand for diesel or other oil products (primarily petrochemicals, industrial fuel, and marine fuel) will be hit any harder than GDP, as demand for these oil products is primarily driven by demand for goods. Although we think gasoline will take a smaller hit (16%) than jet fuel, its large share of global oil demand (26%) means that it is the single-biggest driver of our forecast impact to 2020 oil demand.

How quickly will things return to normal?

We expect a relatively V-shaped recovery for oil demand, in line with our views for economic growth. We expect some lingering impact in 2021 as a vaccine probably won’t be available until midway through the year, but nevertheless the bulk of the lost demand should be recovered by 2021. That’s in line with the rapid demand recovery we project for the second half of 2020. Morningstar forecasts a nearly complete recovery in GDP from the COVID-19 impact, with just a 0.9% impact to the long-term trend of real GDP. Therefore, oil demand should likewise recover nearly to its pre-COVID 19 trend, assuming that the oil intensity of GDP isn’t affected by the crisis.

Our long-term oil-price forecast is unchanged

Our equity valuations incorporate strip pricing for the first two years of our forecasts, and currently the strip is indicating a very weak next two years for oil prices, with prices averaging about US$28 per barrel WTI, or 50% below the 2019 average of $57 per barrel.

Canadian Energy

Canada’s energy sector has been hit as hard as any by the historic crash in oil prices. Earlier this year, the industry was on the verge of rapid expansion as oil sands producers have found a way to generate significant free cash flow with oil prices near US$50/bbl. But with the average oil sands supply cost (excluding transportation) near US$20/bbl, producers are now rapidly burning cash. As such, we expect a meaningful reduction in the country’s crude supply over the next two years, with supply falling from 5.6 million barrels per day in 2019 to 4.4 million barrels per day by 2021.

Our top pick among Canadian energy stocks is Enbridge (ENB) which operates oil and natural gas pipelines. The downturn in oil prices and the expectation of lower Canadian crude supply has renewed fears over Enbridge’s ability to generate sustainable, long-term cash flows and maintain stable dividends because of the potential loss of throughput on the company’s Mainline system. In our view, the market underappreciates Canada’s long-term supply growth opportunities and Enbridge’s cash flow generation potential.

We think that investors are mistakenly worried about underutilization of the Mainline pipeline system due to production cuts and the construction of competing pipeline expansions. Even if the Keystone XL and TransMountain Expansion are placed into service (our base case), we expect only minor underutilization of the Mainline until Canadian crude supply ramps up to our forecast levels once crude prices normalize to our midcycle forecast. Accordingly, we expect all the major pipeline expansions to be operating near full capacity within the next decade, fueled by our above-consensus outlook for Canadian crude production.

Even with the Mainline operating at reduced levels, we expect enough cash flow to cover the company’s coveted dividend. Contrary to popular belief, the Mainline isn’t the only driver of profitability and cash flow generation. Almost 75% of Enbridge’s 2019 adjusted EBITDA was generated from its other assets that are underpinned by secured contracts. Because of this, the dividend looks safe over the next decade