Editor's note: Read the latest on how the coronavirus is rattling the markets and what you can do to navigate it.

The coronavirus has exposed companies that were unprepared and/or unsuited to an economy that is now out of equilibrium. Some impacts are brutal and immediate, business closings, for example. But what about dividend cuts? To what extent are dividend cuts distress signals? And what about when a company that’s consistently paid dividends decides to cut?

For example, last week, Royal Dutch Shell (RDSB) cut its dividend for the first time since the Second World War in response to the plunging oil price and coronavirus crisis. The firm's first-quarter results reveal a staggering 93% decline in pre-tax profit. However, it did not scrap its pay out altogether. The dividend for the first quarter will now be $0.16, down 66% from $0.47 in same period last year. Is this a sign you should head for the hills? Morningstar sector strategist Allen Good doesn’t believe so, saying, “The dividend cut does not impact our fair value estimate or (narrow) moat rating, leaving shares undervalued in our view.”

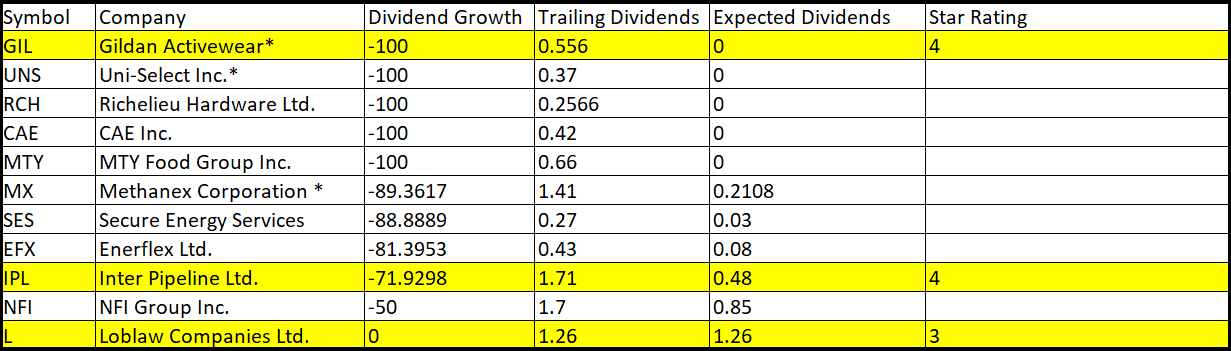

Closer to home, star-rated companies in the iShares S&P/TSX Canadian Dividend Aristocrats Index ETF have been consistently increasing dividends every year for at least five years, though we did find a few that just cut. Here’s a look:

Let’s look at three of these in detail.

Loblaw’s

First up may be one of the few companies we’ve interacted with in this lockdown – so we know for a fact that they’re still in business –grocery chain Loblaw (L). Throughout the crisis they’re delivered sales that analyst Nicholas Johnson describes as ‘eye-popping’. But they’ve held out on declaring a dividend just yet. There are tough times to take into account yet for this company, like costs from temporary wage increases, heightened sanitation, and in-store security to enforce distancing protocols.

“Although sales volumes may be elevated for some time, DBRS Morningstar does not expect to take any positive rating actions in its portfolio of Canadian food retailers solely as a result of the coronavirus due to the offsets of increased costs, a recessionary environment, and increased unemployment,” read a commentary released last Friday on the sector’s credit health. But that’s not necessarily a bad thing.

“Conversely, DBRS Morningstar believes Canadian food retailers are well-positioned to weather this crisis within their respective rating categories. As such, absent of any material disruptions to a food retailer's operations, we do not currently expect to take any negative rating actions in our portfolio of Canadian food retailers as a result of the coronavirus pandemic or the macroeconomic after-effects.”

Morningstar analyst Nicholas Johnson echoed the sentiment, holding his fair value estimate for the company’s stock firm at $71, only having just raised it from $61 on optimism about the firm’s ability to maintain its margin profile.

Inter Pipeline

The next stock is in another industry we’ve seen much of lately, and that’s big oil – Canadian dividend regular, Inter Pipeline (IPL). It might not come as a surprise that with the price of oil, this company has decided to cut its next dividend payout by nearly 72%. But in this case, it seems like a sustainable move for a company that analyst Joe Gemino sees having operating assets thriving in any oil price environment.

“Overall, Inter Pipeline is in a strong position to benefit from growing oil sands production in Canada while rewarding investors with an industry-leading dividend,” says Gemino, noting the still 6% yield, “we see high upside in the stock after the recent slide in commodity prices coupled with the attractive dividend.”

Gildan

Finally, we’ve got Gildan (GIL), not to be confused with Gilead. Demand for their stock has suffeed from the coronavirus and has lost nearly half its value since the start of the year. Their latest earnings missed by more than expected and they’re understandably holding out on a dividend. Gildan moved quickly to cut costs, analyst David Swartz notes, buying this otherwise sustainable Canadian clothing company some time. But in the face of results like 75- and 50-percent drops to sales levels, we’re in unprecedented territory.

“Gildan cut costs quickly in response to the crisis, so its adjusted operating margin of 4.3% nearly met our 4.4% forecast. We expect a large reduction in selling, general, and administrative expenses in the second quarter as Gildan has temporarily shut down much of its production and cut labour costs.”

What does all of this mean?

There are several reasons investors like dividend paying companies. Some may rely on the income stream from dividends to supplement the low yields they are getting from bonds (the historically traditional source of income). Others may simply feel that dividend payers are larger, more stable stocks, which can often be the case especially for consistent dividend payers.

“But remember that in concept, long term buy and hold investors should be indifferent between receiving dividends or allowing the company to re-invest earnings back for future growth, because the end result in your pocket is identical. So before getting up in arms about a dividend cut, have a think about why it is that you own the stock. If it’s for income, perhaps there are other options out there that might be more stable. If it’s for long term capital gains, then maybe allowing the company to manage its earnings during volatile times might not be a bad idea,” points out Morningstar’s Director of Investment Research, Ian Tam.

A dividend cut can be alarming. But in times of crisis, it can show proactive, responsible leadership, often exhibited by those in the business of delivering income. Whether this crisis will let these companies stay in the dividend business is best assessed on a case-by-case basis.

Investing in the low carbon economy

Learn about the companies best positioned to survive and thrive