Stocks endured another rough-and-tumble week: 1,000-point swings in the Dow Jones Industrial Average almost seem commonplace these days.

As a result, the death of former General Electric (GE) CEO Jack Welch flew a bit under the radar. Welch revolutionized the conglomerate during his two-decade reign by aggressively dumping money-losing businesses, acquiring RCA (which included NBC), and growing GE Capital. GE became a profit machine. He was considered by many to be the greatest chief executive of his time.

(History, however, hasn’t been as kind: The firm suffered in the decade after his departure, due in part to some of Welch’s moves: In particular, GE Capital crippled the firm during the 2008 global financial crisis.)

In a nod to Welch, we’re looking at some corporate management teams that we think are doing a good job for shareholders today.

How do we measure that? We think great corporate managers are those who master their roles as stewards of investor capital. Such leaders make investments and acquisitions supporting the competitive advantages and core businesses of their companies--and they won't pay an arm and a leg to do so. They'll divest underperforming or noncore businesses. They'll find the right balance of investing in the business and returning cash to shareholders via dividends and share repurchases. And they'll assemble a portfolio of attractive operating assets and skilled human capital, and then execute well.

We wrap up this thinking in our Morningstar Stewardship Rating for stocks. Morningstar equity analysts assess companies on items such as: financial leverage, investment strategy, investment timing and valuation, dividend and share buyback policies, execution, compensation, related-party transactions, and accounting practices.

Analysts assign one of three stewardship ratings: Exemplary, Standard, or Poor.

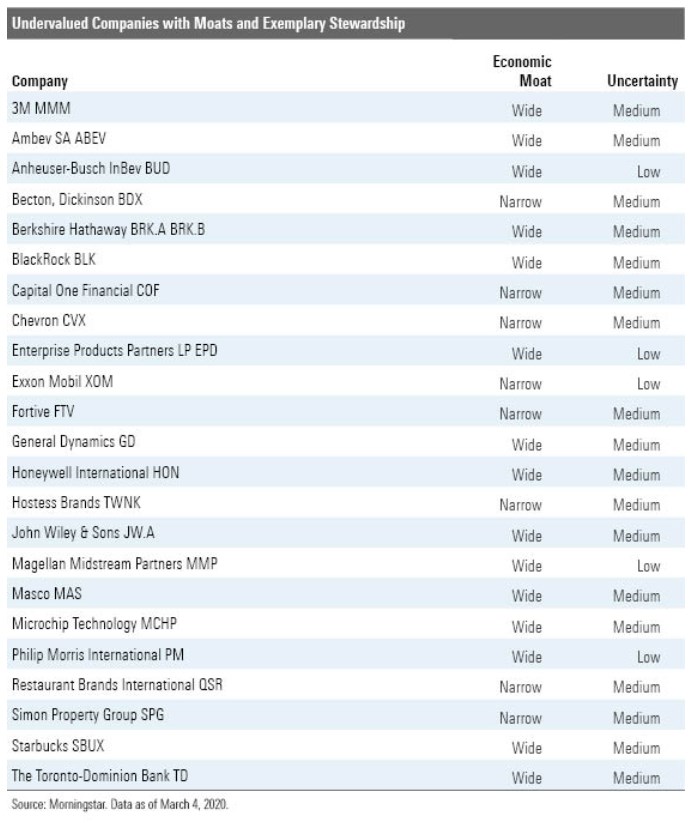

Given the ongoing market unrest, we wanted to focus on exceptional teams leading high-quality, undervalued companies. Specifically, we screened for wide- and narrow-moat stocks with Exemplary stewardship ratings that were trading in the 4- or 5-star range. We tossed out those stocks with fair value uncertainties of high or above.

Twenty-three companies made the cut.

Here’s what our analysts have to say about the management teams at three of the companies from the list.

BlackRock (BLK)

“Larry Fink has been BlackRock's chairman and CEO since the firm first went public in 1999, having run the entities that would eventually evolve into BlackRock since 1988. The company's exceptional stewardship has stemmed from Fink's conviction that for BlackRock to succeed as a publicly traded asset manager it must first act as a responsible, high-performing fiduciary and commit itself to using the company's ever-increasing scale and technological capabilities to deliver value to investors by providing appropriate investments at reasonable prices. Better cultures and internal investment processes, in our view, tend to lead to better and more consistent investment performance, organic growth, and relatively little employee turnover. When growth becomes harder and harder to come by, which has become the case for the more traditional asset managers, we expect firms to take a variety of different actions, including overhauling their leadership or their investment processes, buying a competitor with better performance or greater product, channel, or geographic diversity, or branching out more aggressively into less-exposed strategies. In general, we look positively on firms whose past actions have enhanced their economic moats and have the capital and the wherewithal to maintain their leadership positions and tend to look more skeptically on firms that continue to work on repairing serious deficiencies in their structures or that lack the capital and wherewithal to defend their economic moats longer term.

In an industry where acquisitions have not always worked out, Fink has overseen not one but two major deals--Merrill Lynch Investment Management (2006) and Barclays Global Investors (2009)--that not only transformed BlackRock's business but turned it into the largest asset manager in the world. The MLIM deal more than doubled BlackRock's AUM and altered it from its traditional role as a boutique bond manager into an asset manager that was much more broadly diversified, while still catering primarily to institutional investors. While the BGI acquisition more than doubled BlackRock's managed assets, it did little to alter the company's successful business model even as it transformed the firm from a primarily active asset manager to a major provider of passive products. These two deals not only added to BlackRock's existing product lineup but expanded its footprint into other channels and markets and left the firm agnostic to shifts among asset classes and investment strategies.

A major reason BlackRock has had success with acquisitions where so many have failed is that Fink has insisted on one culture for the firm--commonly referred to as One BlackRock--which has been reflected in the level and consistency of the company's investment performance, its rate of organic growth, the focus and importance that has been placed on risk management, and the limited amount of voluntary employee turnover. We continue to be impressed by efforts BlackRock has made to broaden the scope of its senior management team and groom potential successors for Fink and president Robert Kapito by moving key personnel around into different management roles, with a small group of top leaders at the firm receiving equity incentive grants, which vest over a period of five to seven years, as BlackRock looks to retain and develop its bench of senior executives. While there is no indication that either Fink or Kapito is going anywhere anytime soon, we think it is prudent for the board and senior management to be taking these steps. The firm's exceptional record with capital allocation, as well as this preparation for the eventual departure of both Fink and Kapito by strengthening the skill set of the company's wider management team, is supportive of our Exemplary stewardship rating.

That's not to say that there haven't been cracks in BlackRock's armor--like the poorer performance of the firm's actively managed funds during the past decade. With $1.947 trillion in AUM at the end of 2019, BlackRock's actively managed fund operations are one of the largest in the world. This business generates 46% of the company's base management fees, despite accounting for 27% of long-term AUM. Following poor investment performance in the aftermath of the 2008-09 global financial crisis, which affected flows for both its active equity and fixed-income platforms, BlackRock started bringing in new managers and introducing different ways of processing and organizing its investment teams in 2012. While this led to improved performance in BlackRock's actively managed fixed-income and equity platforms, which is the first step toward putting these offerings in a better position to generate positive flows, results have been inconsistent. In March 2017, the firm moved more than 10% of its active equity strategies into more quantitatively based strategies, a sign that management's patience is not infinite.”

-Greggory Warren, strategist

Microchip Technology (MCHP)

“We view Microchip as a well-run organization and an Exemplary steward of shareholder capital. Microchip is led by longtime CEO Steve Sanghi. We think that Microchip has done a stellar job of distributing cash to shareholders. The firm has a very attractive dividend policy, paying out over half of its earnings and increasing the dividend (albeit in tiny amounts) on a quarterly basis. We believe that Microchip's management team understands the importance of its dividend as part of an investment thesis.

The company has also made reasonable moves on the M&A front; acquisitions of Silicon Storage Technology, Standard Microsystems, ISSC, and Supertex involved buying only the pieces of each firm that either generate, or have the potential to generate, strong profitability, while spinning off less desirable product lines that would weigh on the firm's returns on capital. Microchip's largest deals, to acquire Micrel Atmel and, most recently, Microsemi, have followed a similar disciplined playbook. The Atmel deal put Microchip into a net debt position, but the firm earned better-than-expected accretion from the merger. Microsemi leverages up the Microchip balance sheet to a greater degree, but again, we anticipate healthy synergies, rapid deleveraging, and ultimately expect it to be another good deal made by this exemplary management team.

Furthermore, on the M&A front, Microchip has walked away from potential deals that no longer made financial sense, such as its failed bid to acquire CSR, which was eventually acquired at a higher price by Qualcomm. Ultimately, Microchip has further room to expand its product portfolio and become more of a one-stop shop in the chip market, similar to Texas Instruments today, and we foresee further acquisitions at reasonable valuations over time.”

-Brian Colello, director

Simon Property Group (SPG)

“We assign Simon Property Group an Exemplary stewardship rating. CEO David Simon has been with the company since 1990, becoming president and directing the initial public offering in 1993, becoming CEO in 1995, and then becoming chairman of the board in 2007. Brian McDade was promoted to CFO at the end of 2018, adding the position to his role as treasurer, which he has served at Simon for the past 14 years. President and COO Richard Sokolov has been with Simon since 1996, previously serving in multiple executive roles and finally as CEO of DeBartolo Realty, a mall REIT purchased by Simon in 1996. The board of directors is made up of primarily independent, well-accomplished members who are elected annually. The experience of the management team gives us confidence that the company will continue to make smart capital decisions and source accretive development projects.

Simon Property Group has a long history of acquiring and developing high-quality malls and has delivered shareholder returns that have beaten the S&P 500 and REIT indexes over the long term. Simon was founded in 1960 by brothers Melvin Simon and Herbert Simon as a developer of high-quality malls. After going public, the company began utilizing its access to equity capital to acquire competitors that owned other high-quality assets. Acquisitions include rival DeBartolo Realty in 1996, Retail Property Trust and Corporate Property Investors in 1998, Rodamco North America in 2002, Chelsea Premium Outlets in 2003, Mills in 2007, and most of Prime Retail and Capital Shopping Centers in 2010. Simon also tried to acquire Class A mall REIT peers GGP and Macerich in 2010 and 2015, respectively, though its bids were ultimately rejected. Simon spun out its smaller and lower-quality malls into mall REIT Washington Prime Group in 2014 to focus on Class A malls, shedding the company of the assets that would struggle to compete with e-commerce.

Simon Property Group in 2020 entered into a definitive agreement to acquire 80% of Taubman Centers for US$3.6 billion. Taubman Centers owns 26 high-quality retail properties, including 21 malls throughout the U.S. and three malls in Asia. We have a very favorable view of Taubman's portfolio of Class A malls, with Taubman reporting same-store sales per square foot of US$972 in the fourth quarter of 2019, which should significantly improve Simon's average portfolio quality given that Simon reported US$693 for the fourth quarter. We like the deal for Simon for many reasons. The deal was done at a 6.2% cap rate and this makes this deal immediately accretive to earnings. The deal further cements Simon's status as the premier Class-A mall owner, which should give it further leverage in negotiations with retailers looking to place stores in its highly sought-after portfolio. Finally, the Taubman locations should provide profitable locations for Simon's recent investments into several major retailers that management can easily control. We appreciate that Simon was able to take advantage of the public market's mispricing of Class A malls to acquire one of the top mall portfolios at a very attractive price.”

-Kevin Brown, analyst

.jpg)