Canada is great. Its contributions to global culture cannot be denied, from a seemingly endless list of acting and musical talent, innovations like the Robertson screwdriver and the egg carton, to the invention of sports like basketball and ice hockey. Our great nation, filled with diversity and inclusion, is a place that many are proud to call home.

But there also are less rosy aspects that cannot be ignored, especially for investors – and even more so for retail investors. Unfortunately, Canada is also home to an environment of high fees. In Morningstar’s 2019 Global Investor Experience study focusing on Fees and Expenses, it was calculated that the asset-weighted median expense ratio for equity funds was close to 2%, one of the highest among 25 other developed countries.

Fund fees are expressed on an annual basis but are typically charged monthly or quarterly. For most funds, fees are charged regardless of how the investment manager performs. Assuming an overall cost of 2% to own a fund, if in one year a fund returns 6%, you’ll receive roughly 4% for that year. However, if the fund loses 6%, you lose 8% after fees. That’s right. You will probably pay the same fee this year as you did last year on the same fund that in all likelihood is showing losses on a YTD basis.

The power of compounding

Though perhaps not financially impactful in a single year, over time the effects of fees are substantial.

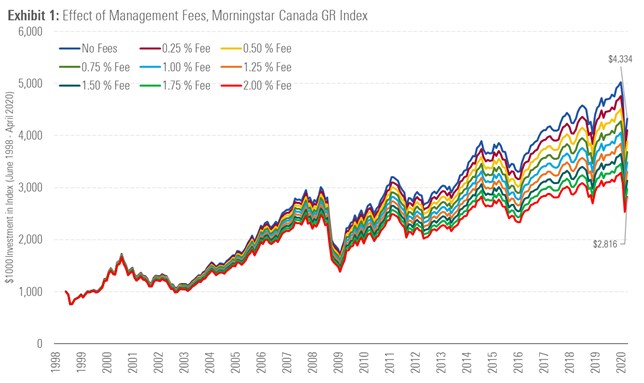

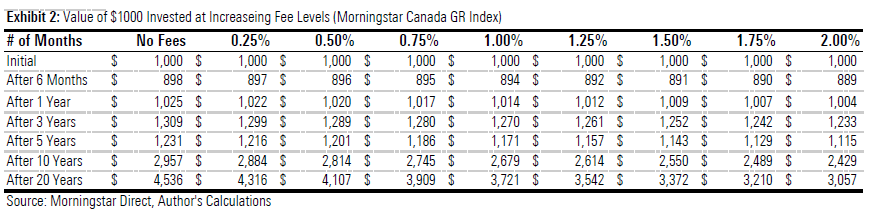

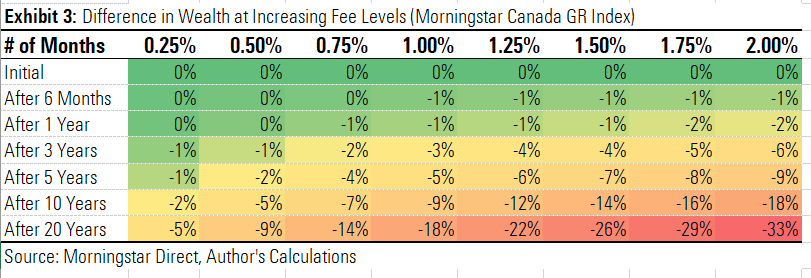

Source: Morningstar Direct, Author’s calculations

In this example, the blue line shows the performance of the Morningstar Canada GR Index, which represents a market-cap weighted portfolio of 220 Canadian-listed companies. Below that are representations of the same index but with an annual fee applied ranging from 0.5 % to 2%, charged monthly. As time passes, the gap between the index and the fee-laden representations widens dramatically.

In dollar terms, a $1000 invested in the index in 1998 results in a portfolio value of $4,500 after 20 years if there were no fees, but only $3000 if a fee of 2% was charged.

Put in percentage terms, after 10 years, the impact of a 2% fee results in a difference of 18% less wealth when compared to no fees. After 20 years, that gap balloons to 33% So you need to be diligent in monitoring the fees you’re being charged, because the fees you pay are detrimental to the amount of wealth you will end up with.

Different fees for different share classes

Most retail mutual funds are available to investors through different share classes. A single fund offered through different share classes gives the investor exposure to the identical portfolio of stocks and bond regardless of which share class is purchased.

A-class shares are the most expensive in terms of explicit fees but have the cost of advice embedded into them.

F-class shares are available specifically through a fee-based advisor account and have fees that are listed lower but don’t include the overall management fee. The advisor usually charges a management fee separately, for managing the portfolio on a discretionary basis. Typically, fee-based accounts are reserved for those with larger account sizes. They are often better in aligning investor interests with the advisor, since no individual transaction fees are charged by switching funds. This encourages focus on maintaining a sound investment process and discourages ‘churning’ of the account for commissions.

Finally, D-class shares are those that are made available through discount brokerages, and do not come with any advice.

It is worthwhile to look at the types of funds that you hold within your overall portfolio, perhaps asking the question whether there are lower fee share classes available to you, or if you are eligible to pursue a fee-based account.

Good advice is valuable

The value of advice is decidedly worthwhile, and Morningstar has quantified this in the past. However, it is only worthwhile if you actually get good advice. Unfortunately, an Ontario Securities Commission’s Investor Advisory Panel survey of 3000 Canadians who are paying fees for advice found that “31% were unable to say their advisor had ever spoken to them about planning for financial goals such as retirement, education or buying a home.”

Along with financial planning for major life events, financial coaching through volatile market periods like the one we’re in right now are paramount to investors to help avoid making poor investment decisions based on gut reactions and emotions. The point here is that the embedded fees in funds pay for the advice that you should be receiving as in investor. Consider using it more regularly, and in particular in helping to navigate through uncertain times.

:quality(80)/cloudfront-us-east-1.images.arcpublishing.com/morningstar/OSPGGQHXJVCGLBHR5CUUQWH3NQ.png)

:quality(80)/cloudfront-us-east-1.images.arcpublishing.com/morningstar/ZHTKX3QAYCHPXKWRA6SEOUGCK4.png)