See more episodes of Quant Concepts here

Phil Dabo: Welcome to Quant Concepts' working from home edition. The NASDAQ got a lot of attention last year because it generated an outstanding calendar year return of 45%. The U.S. tech sector was without a doubt one of the largest contributors to that outperformance and also had a return of around 45%. On the other hand, the Canadian tech sector hasn't gotten nearly as much attention as its American counterpart but had a remarkable return of 81%. Although the Canadian tech sector doesn't have nearly as much depth as the American one, it can still add meaningful alpha to your portfolio.

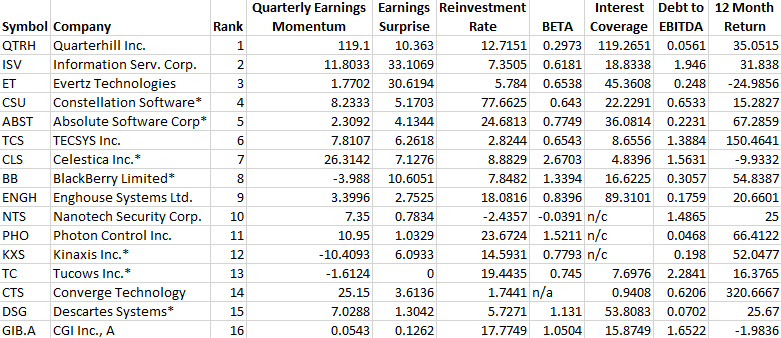

Today, let's take a look at a strategy that focuses on Canadian tech companies. We're going to start by selecting our universe of stocks. In this case, it's all of the Canadian stocks in the CPMS database. Today, that includes 46 stocks, and we're going to rank those thoughts from 1 to 46 according to four key factors. Three of these factors are based on corporate fundamentals that I would like to see in tech stocks.

I want stocks that have good quarterly earnings momentum and earnings surprises. Not only do I want to see stocks that have increased their quarterly earnings, but I also want to see that they've beaten analysts' expectations. These are both shorter-term metrics. Next, I want a really good reinvestment rate based on earnings per share. Ideally, I would like to see tech companies with good earnings and the ability to reinvest those earnings into profitable opportunities. The last factor is beta because I would like companies that are not as correlated to the S&P/TSX.

Now, let's take a look at our buy rules. We're only going to buy stocks that are ranked in the top half of our list. I want to exclude stocks that are at the bottom of our list based on the interest coverage ratio. Interest coverage is used to determine how easily a company can pay its interest expenses on outstanding debt. This is important for tech stocks that are taking on more debt in order to aggressively grow their business. We're also going to exclude stocks that are at the bottom of our list based on debt to EBITDA. This is a metric that is frequently used by credit rating agencies and used by banks when providing business loans. It can reveal how capable a company is of generating sufficient income from operations in order to service and pay for debt.

Now, let's move on to our sell rules, and in this case, we've kept our sell rules very simple. We're going to sell stocks that fall out of the top 60th percentile of our list, and we're also going to sell stocks if their debt to EBITDA deteriorates and falls to the bottom of our list.

Now, let's take a look at performance. The benchmark that we used is the S&P/TSX Technology Total Return Index, and we tested this strategy from January 2005 to December 2020. Over that period, this strategy generated a very strong return of 17.5%, which is 8.4% more than the index and a very high annualized turnover of 100%.

When taking a look at the annualized returns, we can see that this strategy generated a very strong absolute return over every calendar period but didn't necessarily beat the index over shorter time periods. When we take a deeper look at performance, we can see that the strategy only had one negative calendar year since 2005, whereas the benchmark had five calendar years of negative returns. Two of those periods included a return of less than 50%.

When taking a look at the price risk of the strategy, we can see that the standard deviation is much less for the strategy. Also, when looking at the risk-adjusted returns as measured by the Sharpe Ratio, the strategy had very good performance. It's not surprising that the market risk as measured by beta is lower for the strategy.

I really like this chart showing very strong outperformance by the strategy, and I think it's important to note that there have been periods in calendar year returns that are higher than 40%. I also like to look at the market capture ratios because the overall market capture ratio is very strong, and this is a strategy that has performed well in down markets as you can see by the downside capture ratio.

This is a great strategy to consider if your portfolio is tilted towards companies on the S&P/TSX and you're looking to add some alpha to your portfolio. In addition to that, this strategy focuses on companies that have stronger fundamentals. The strategy overall has a higher turnover and it has a tendency to pick up both small and microcap stocks, but it does a great job of finding companies that are not widely owned by investors. You can find the buy list along with the transcript of this video.

From Morningstar, Phil Dabo.

Capture Opportunities in New Technologies

Learn about the Morningstar Exponential Technologies Index here

.jpg)