One of the reasons I love living in Toronto is we have four distinct seasons. Winter is cold, summer is hot, spring is usually wet, and autumn is always beautiful. Coming from Mumbai – where we just alternate between rainy and hot, I like the certainty. It helps me plan, and when I know what to expect.

Because I like predictability, I look for patterns. I’ve noticed certain themes crop up a lot in financial circles. Dividends, for example, is a perennial favourite topic. Retirement, and FIRE, are two other topics of interest, especially around December and February. And every few months, like clockwork, I can expect to see horror stories around pooled registered education savings plans, or Group RESPs.

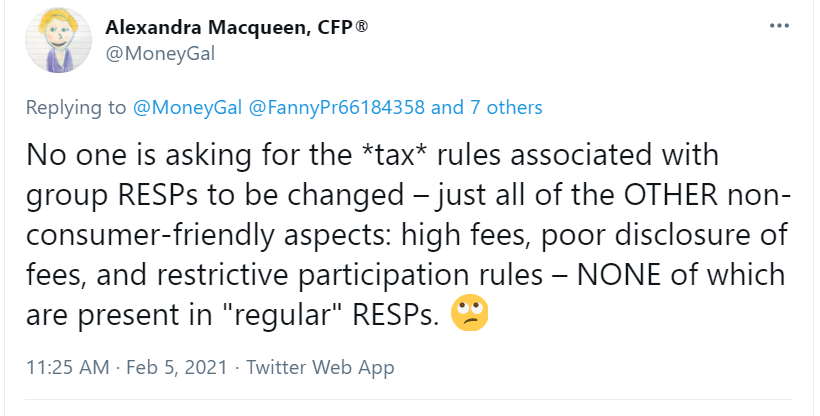

The latest instance was last week when Ellen Roseman initiated a discussion on Twitter. A lot was going on in that discussion, one tweet by Morningstar contributor Alexandra Macqueen caught my eye. It says:

Macqueen is right when she says that they’re not consumer-friendly at all. They have high fees, the disclosures on what the fees will actually cost you are poor at best, they are complex and difficult to understand, the rules to participate are restrictive, and it is extremely easy to get kicked out and lose a lot.

Right at the outset, let me say that I don’t think that group RESPs are a con game. In fact, if you participate as planned, and see the plan through to the end, and then your child pursues a post-secondary education as expected…and all this happens in the time-frame you expect when you initially invest in the plan around a decade before all of this comes to pass, then sure. They work well.

Think about that for a second, though. If someone told you in January of 2020 exactly what you could expect in January of 2021, would you believe them? Yet, group RESPs require you to make these assumptions about your child’s decisions and future, years, sometimes decades in advance.

A 2008 Review of Registered Education Savings Plan Industry Practices Report prepared for Human Resources and Social Development Canada says, in no uncertain terms, “In all, there is a significant risk that participants in group plans end up in a worse financial situation as a result of their participation. These participants may be discouraged from saving again or from enrolling in post-secondary education. Such outcomes are not in accordance with education saving policy objectives.”

What Are Group RESPs?

Group RESPs are also called scholarship trusts, or pooled plans, and are sold only by scholarship plan dealers. They are different from other RESPs. In Group RESPs, you have a contractual agreement to buy a set number of plan units, which then represent your share of the plan. Your plan matures based on your child’s birth date.

Most importantly, you will have a schedule based on which you need to make regular contributions to the plan. The manager of the group RESP will invest your contribution, along with the contributions from others in your plan. Your child, or the beneficiary of the plan, will share in the pooled earnings of investors with children of the same age (that is why the maturity is based on the child’s birth date).

How much does your child get? The short answer is, “It depends.” Several factors impact eventual payout, including the amount in the group account, the number of children in the group who will be starting post-secondary education, and whether your child begins post-secondary education at the same time as the group, among others.

What are the Fees?

Different RESP providers and plans have different rules and fees. Some of the larger providers are Knowledge First Financial (which owns Heritage Education Funds), Canadian Scholarship Trust Plans and Kalaido (which used to be called Universitas).

According to Heritage Education Funds’ 2020 Prospectus, the sales charge is $100 per unit (pro-rata basis for fractional units). The sales charge is deducted from early contributions as follows: 100% of your contributions go towards the sales charge until half of it is paid.

This is key. Because it means that if you cancel your plan in the first few years, you’ll get back much, much less than you put in.

The prospectus also points out that after that, 50% of your contributions go to pay off the sales charge and 50% is invested in your plan. Depending on the contribution schedule you selected and the age of your beneficiary, the sales charge may range between 2.47% and 22.86% of the total cost of the unit.

In the case of Canadian Scholarship Trusts, the sales charge is higher. The prospectus notes that this can be between 3.1% and 24.1% of the cost of a unit.

Also remember, this is just the sales charge. You also have opening fees, management fees, maintenance fees, and transaction fees, including withdrawal fees, transfer fees, bank charge fees, and charges for any changes you might make, including contribution changes, or beneficiary changes.

Upon maturity, your beneficiary – usually your child, though sometimes it could be the child of a friend or your grandchild – will be paid only if he or she enrolls in eligible studies. Most providers offer a list of eligible programs. Here is the list from Knowledge First, as an example. If not, you’ll have to change the beneficiary (fees apply) or transfer the money out (fees apply) or withdraw (taxes and fees apply).

What If I Stop?

The most important thing to remember here is that if you stop contributing, the amount you get back is always less than the money you put in because you will get your contribution back minus fees. You may also forfeit any earnings you may have because your earnings remain in the plan to be divided among the surviving plan members.

There are many examples of parents getting nasty shocks. This parent contributed $65 per month for several months, contributing a total of $568. The principal in her account after fees? $66. This deep dive highlights many cases where parents have lost thousands. This parent tried to transfer $3,000 from a group RESP and found that it would cost her $2,000 in fees to do so.

On the flip side, if you stay in the plan until it matures, your child may share in the earnings of those who left the plan early.

All of this is confusing, and the one question that remains is, if you decide to not go the group RESP route, what should you do?

What Should I Do?

A few years ago, Wendy Stein, a product manager at Morningstar Canada, had the same problem. She came up with a strategy to invest in her children’s education with four criteria.

- Low cost

- Low minimum initial purchase

- Attractive total return and risk/reward profile

- A "set it and forget it" investment.

She ruled out group RESPs for the obvious reasons. She also ruled out exchange-traded funds because she didn't want to pay transaction costs for a periodic purchase plan and reinvestment of distributions. (Note: This strategy as written a few years ago. Now, many brokerages wave commissions on the purchase of ETFs). For Stein, her investable universe consisted of mutual funds.

She made a list of Series D funds that allowed a $500 or less minimum initial purchase. Seried D funds usually have lower management expense ratios. This took care of points one and two on the list. For point three, an attractive total return and risk/reward profile, she used the Morningstar Rating as the first step in my fund-evaluation process. The Morningstar Rating gives investors the ability to quickly and easily identify funds that have superior historical risk-adjusted returns and are worthy of further research. She screened for funds with a rating of 3-stars or better. Finally, she narrowed her list to only target-date funds, and chose the ones that would make sense for her time horizon.

Some Target Date Fund Options

As Morningstar’s Director of Investment Research Ian Tam points out, the combination of the tax-shelter provided through an RESP and well-selected a target date fund can provide a reasonable dent into future debt. At a high level, target date funds are products that invest in multiple asset classes (stocks, bonds, cash), and dynamically change the mix between these asset classes over time.

Why not just buy the index? “In a word – timing. If your kids are young and you don’t anticipate needing the capital invested for 10+ years, historically you would have been better off investing in an index, even after withstanding the deep drawdowns of the pandemic. However, if you had started investing a few years ago, the picture would look quite different,” Tam notes.

If you’re wondering how to pick a target date fund, one helpful guide is in the name. For example, if you anticipate that your child will go to college in 2030, then look for a fund with ‘Target Date 2030’ in its name. Here is a list of 4-star Target Date Funds:

| Name | Morningstar Category | Distribution Channel (Canada) | Morningstar Star Rating | 5-yr Return |

| PH&N LifeTime 2025 Fund D | Canada Fund 2025 Target Date Portfolio | Do-It-Yourself | 4 | 6.65 |

| BMO Target Education 2025 Portfolio D | Canada Fund 2025 Target Date Portfolio | Do-It-Yourself | 4 | 6.11 |

| RBC Target 2030 Education Fund D | Canada Fund 2025 Target Date Portfolio | Do-It-Yourself | 4 | 7.75 |

| RBC Target 2025 Education Fund D | Canada Fund 2030 Target Date Portfolio | Do-It-Yourself | 4 | 6.11 |

| PH&N LifeTime 2030 Fund D | Canada Fund 2030 Target Date Portfolio | Do-It-Yourself | 4 | 7.65 |

| PH&N LifeTime 2035 Fund D | Canada Fund 2035 Target Date Portfolio | Do-It-Yourself | 4 | 8.37 |

Source: Morningstar Direct | Data as of February 5, 2021

Individual details for each of these funds can be found on the fund pages - linked above. The MERs for each of these funds is in the range of 0.96% to 1.16%, Remember that the Morningstar Star Rating is a historical measure of risk-adjusted returns after fees against the category to which the fund belongs. It is also important to note the distribution channel. Do-it-yourself share classes are sold primarily through discount brokerages and do not include fees for advice.

.jpg)