The Canadian Registered Retirement Savings Plan (RRSP) contribution deadline for the 2021 tax year is coming up soon. If you’ve been diligently contributing to your plan over the year, kudos to you! Given that 2021 marked a year of elevated savings for Canadians, it is very possible you might have a bit of extra cash to squirrel away for retirement. Where should you put it?

Today, we highlight some mutual fund options for your retirement portfolio. To being with, investors must understand how much risk they can take on, which in large is a function of your risk profile and your time horizon. In very simplistic terms, the more risk you can take on, the more you can afford to invest in stocks as opposed to bonds.

This said, the broad majority of mutual fund investors in Canada tend to have assets in balanced funds, which are “all-in-one” type products which target specific allocations to stocks and bonds. Many providers offer families of products with varying asset allocations suited for different investor profiles. Investors who seek an ‘all-in-one’ solution would do well in considering one of these products, since they re-balance regularly and keep a sharp eye on the asset mix without much work from the investor.

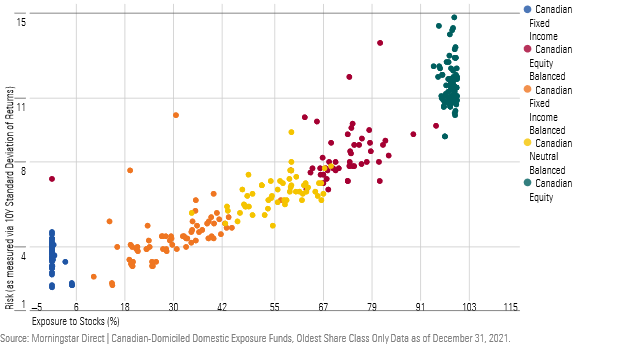

This scatterplot depicts all the balanced mutual funds available to Canadian investors (as categorized by the Canadian Investment Funds Standards Committee, currently chaired by Morningstar), that invest only in domestic stocks and bonds. As exposure to equities increases, so too does the risk. It is vitally important that you as an investor choose the right mix that is suited to your financial situation. Investors who are nearing retirement and likely cannot take as much risk will likely skew to funds on the left side of the chart, while young investors who have a long career ahead of them may opt to skew to the right.

To find some reasonable suggestions in balanced categories, we ran a screen for funds that met two requirements:

First, they’ve received a Morningstar Star Rating of 5 stars. The Morningstar Rating for Funds, or the Star Rating is an objective lookback at how funds have performed against their category peers, on a risk-adjusted basis, after fees. Though they are a lookback, our data indicates that after the fact, 5-star funds are more likely to outperform their peers than 1-star funds. In other words, good managers tend to continue to be good managers, while poor managers continue to do poorly in many cases.

Second, they’ve received a Morningstar Quantitative Rating of Silver or Gold. The Morningstar Quantitative Rating is our assessment of a fund’s ability to outperform peers in the future, based on our analysis of the parent company, the people running the fund, and the process used.

The funds that meet the above criteria are listed in the table below. The list includes funds that have a global mandate, which is a worthwhile consideration, especially if you are guilty of home country bias. Where available, fee-based or do-it-yourself share classes of funds are listed, which exclude the cost of advice. Fee-based mutual funds are sold through advisors that will typically charge an overall management fee outside of the MER listed below. D-class mutual funds are available through discount brokerages and offer no accompanying advice.

|

Name |

MER (%) |

MQR |

3-yr Returns |

5-yr Returns |

10-yr Returns |

|

Canadian Equity Balanced |

|||||

|

1.00 |

Gold |

13.3 |

8.0 |

7.2 |

|

|

0.86 |

Gold |

12.5 |

7.7 |

9.3 |

|

|

1.13 |

Silver |

12.2 |

9.3 |

|

|

|

Canadian Neutral Balance |

|||||

|

1.09 |

Silver |

8.7 |

7.0 |

8.7 |

|

|

0.89 |

Silver |

9.8 |

7.2 |

|

|

|

0.91 |

Gold |

8.9 |

7.2 |

8.6 |

|

|

1.05 |

Silver |

9.5 |

7.0 |

7.0 |

|

|

0.85 |

Gold |

10.2 |

7.4 |

7.5 |

|

|

1.11 |

Silver |

9.1 |

7.2 |

|

|

|

Canadian Fixed Income Balanced |

|||||

|

0.74 |

Silver |

6.9 |

5.2 |

5.2 |

|

|

1.12 |

Silver |

7.1 |

5.2 |

|

|

|

Global Equity Balanced |

|||||

|

1.12 |

Silver |

8.4 |

8.6 |

10.0 |

|

|

1.10 |

Silver |

10.5 |

9.1 |

|

|

|

1.09 |

Silver |

16.6 |

13.6 |

11.0 |

|

|

1.18 |

Silver |

10.2 |

8.5 |

8.5 |

|

|

1.28 |

Silver |

12.1 |

9.9 |

9.8 |

|

|

1.16 |

Silver |

11.9 |

10.0 |

11.1 |

|

|

1.15 |

Silver |

12.7 |

9.7 |

10.5 |

|

|

1.14 |

Silver |

10.7 |

9.2 |

|

|

|

0.98 |

Silver |

10.4 |

8.9 |

|

|

|

1.23 |

Silver |

10.7 |

8.4 |

8.4 |

|

|

Global Fixed Income Balanced |

|||||

|

0.92 |

Silver |

7.0 |

5.6 |

6.7 |

|

|

0.74 |

Silver |

6.5 |

5.1 |

|

|

|

0.90 |

Silver |

7.7 |

5.9 |

6.4 |

|

|

Global Neutral Balanced |

|||||

|

0.84 |

Gold |

8.9 |

7.9 |

|

|

|

1.11 |

Silver |

11.0 |

9.6 |

8.7 |

|

|

0.96 |

Silver |

9.7 |

8.8 |

|

|

|

1.14 |

Silver |

9.8 |

9.2 |

|

|

|

1.22 |

Silver |

13.1 |

12.2 |

9.2 |

|

|

1.14 |

Silver |

10.4 |

8.1 |

|

|

|

0.92 |

Silver |

14.2 |

10.8 |

|

|

|

1.14 |

Silver |

14.0 |

10.6 |

|

|

|

0.92 |

Gold |

8.2 |

7.3 |

9.1 |

|

|

0.89 |

Silver |

8.1 |

7.2 |

9.0 |

|

|

0.94 |

Silver |

9.0 |

7.3 |

9.7 |

|

|

0.82 |

Silver |

10.7 |

8.9 |

11.1 |

|

The universe of mutual funds available of course is much, much larger. However, for the broad majority of Canadians who wish to invest their hard-earned in a reasonable fund that requires little work, the above might be a good place to start further research.

All this said, over time as you age, your ability to take on risk diminishes as you near retirement. Though balanced funds are great over long stretches, as an investor you will need to be conscious of when your risk profile shifts enough to warrant a change in product. Sure enough, the fund industry has a solution for this as well.

Target date funds are a type of balanced fund that invests your assets in a ‘glide path,’ slowly reducing your exposure to stocks as you get nearer to the time you retire or require your investment assets (aka the target date, which is usually in the name of the fund), thereby reducing risk gradually to match your risk profile. BMO, Fidelity, IA Clarington, Invesco, RBC, and Sunlife are examples of Canadian-domiciled fund providers that offer target date products in mutual fund format.

This article does not constitute financial advice.