Investors can be excused if after this week’s U.S. Federal Reserve meeting, they feel a bit like Charlie Brown after Lucy pulls the football away.

Markets headed into the Fed meeting on watch for signs of a “pivot” away from an unprecedented series of aggressive interest-rate increases, and perhaps a sense that the Fed was starting to think about an end to raising rates. That hope had helped lift stocks during their October rally from September bear-market lows.

That wasn’t to be the case.

It may well be that at the next Fed meeting in December rates won’t be increased by as much, analysts say. But the takeaway was that until inflation shows sustained signs of heading lower, rates are heading still higher and will stay that way for a while.

For the stock and bond markets, that means the coast isn’t clear yet. The lows for stock prices may not yet be in, and for some parts of the bond market, yields may still head higher.

“The market and investors keep looking at the Fed to signal that rate increases are done and it’s the ‘all clear’ signal,” says Kevin Holt, chief investment officer for U.S. value equities at Invesco. But when it comes to a determination to fight inflation, “the Fed has been pretty consistent, even if the market doesn’t want to acknowledge that.”

When it comes to inflation, he says, “the Fed is going to stay on point until it sees the whites of the eyes.”

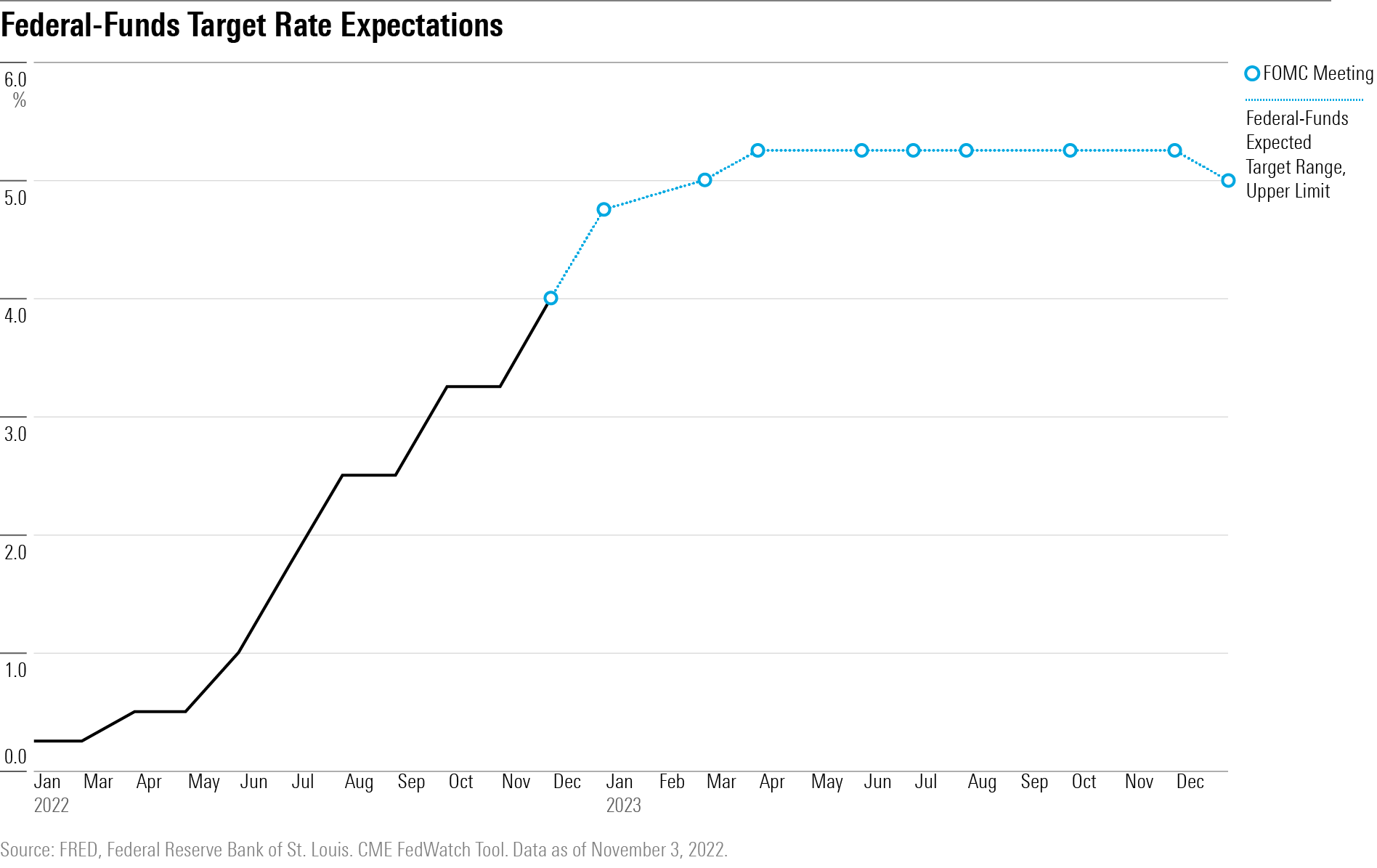

Rate Expectations Go Still Higher

On Wednesday, the Fed announced it was raising the federal-funds rate target by another 0.75 percentage points to a target range of 3.75%-4.00%. This was the fourth consecutive rate hike of three-quarters of a point, an unprecedented pace of interest-rate increases.

But what got investors’ attention were comments by Fed Chair Jerome Powell when he spoke to reporters following the policy-setting Fed meeting. “It’s very premature to be thinking about pausing rate hikes,” he said. “We have a ways to go.”

The result was that, as has repeatedly been the case this year, following the Fed meeting the bond market once again ratcheted up expectations for how high the Fed will ultimately have to raise interest rates.

The Fed is now expected to take the federal-funds rate toward a target rate of 5.25%-5.50% in early 2023, according to the CME FedWatch Tool. A month ago, the Fed was expected to stop raising rates when it hit a target of 4.50%-4.75%. (For Morningstar’s take on the outlook for Fed policy, see our latest update here, and for the latest stock market outlook, visit here.)

The Fed “wants to make sure they don’t make the mistake of failing to tighten enough or loosening policy too soon,” says Bob Michele, chief investment officer and head of the global fixed income, currency & commodities group at J.P. Morgan Asset Management.

Given inflation is continuing to trend at a very high levels, Powell “has to talk tough,’’ Michele says. However, he does expect the Fed to slow the rate of increases at the December meeting with a 0.50-percentage-point boost to the funds rate amid signs of a slowdown in housing and some corporate earnings.

But ultimately, Michele says, the Fed won’t stop raising rates until the funds rate is above the rate of inflation. (Michele says he measures this by looking at a rolling three-month, annualized rate of inflation as measured by the Consumer Price Index, excluding food and energy.) “I don’t think the Fed will have to go to 7% or 8%,” he says. “I think by the time they get to 5% or 5.50% in the first quarter, inflation will have dropped below that level,” allowing the Fed to pause its rate hikes.

Pivot vs. Pause

For investors, it’s critical to understand the difference in what has become known as the “pivot” versus “pause” discussion in the markets.

With a “pause,” the Fed will stop raising rates and assess the impact of the rate hikes it has done so far on the economy and the direction for inflation. “To us a pause is the Fed saying, ‘We’ve done a lot in a short period of time and we’ve gotten to some target,’” Michele says. If inflation has started to slow, “maybe they are done, but if it doesn’t, they will start hiking again.”

A “pivot,” meanwhile, “is the Fed saying ‘We’ve done enough and that’s it, no more rate hikes and we’re looking for an opportunity to cut rates,’” Michele says. That could mean holding rates above 5% for a year, he adds, even if the next move is to swing the focus from inflation-fighting to stimulating economic growth.

How Deep Would a Recession Be?

With Powell’s message, a critical variable for stock and bond markets is how deep any recession will be. Preston Caldwell, Morningstar’s chief U.S. economist, says that asking if there will there be a recession “misses the point.”

Tom Porcelli, chief U.S. economist at RBC Capital Markets, says Powell is a “Fed chair who’s clearly on a mission to kill inflation. The problem is, he is going to ding the economy in the process. And probably pretty aggressively.”

Porcelli says the expectations have generally been for a shallow economic downturn in 2023. “Now, I think everyone’s really rethinking is it really going to be that shallow? Is it going to be shallow at all?”

A deeper recession will likely lead to a more significant decline in corporate earnings, which likely means continued declines for stocks but perhaps a better environment for government bonds. A shallow recession could mean that corporate earnings could remain healthier and minimize additional losses for stocks.

What’s Next for the Stock Market?

While stocks have bounced from their most recent bear-market lows set in September, Invesco’s Holt is skeptical that the rebound can hold.

Underlying that belief is an expectation that the outlook for corporate earnings is still too optimistic, and that if earnings forecasts are reduced, stock prices will follow. He sees stocks having the potential to fall 10%-19% from current levels, as measured by the S&P 500.

In particular, Holt expects a continued rough ride for technology stocks. Among many of the tech stocks that led the bull market higher, “they are in the maturation stage of their business models,” he says. Previously, even as the economy slowed, because companies would still be gaining market share, their stocks could remain buoyant.

Holt says investors should brace for a scenario broadly among technology companies similar to the experience following the dot-com bubble collapse. “Just like there was after 1999, you had maybe 75% of companies that didn’t make it, but there were those 25% that did.”

He also expects an earnings slowdown beyond tech stocks. “I think we will see a very tough Christmas, and retailers, which have already been hit, will continue to get hit,” Holt says. Even among energy stocks, which have buoyed the market in 2022 and helped keep third-quarter earnings in positive territory, growth will likely slow down next year, he says. “If energy prices flatten out, energy companies will be ok … but aren’t going to lift the market.”

Still, Holt sees the market favoring companies with strong cash flows. And as we head into the middle of 2023, as long as the Fed is able to stop raising interest rates, the focus will start to turn toward an economic rebound. At that point, cyclical stocks should come back into favor, including tech companies that have a strong advertising focus. Banks, too, should benefit as continued high interest rates will favor net interest margins on lending businesses, he says.

What’s Next for the Bond Market?

J.P. Morgan’s Michele says that in the Treasury market, the majority of the rise in yields—and decline in prices—is history. “If I think about where we started, we have probably had 80%-90% of the increase in Treasury yields we’re going to see.”

Still, Michele says the yield on the U.S. Treasury two-year note will rise to about 5.0% from its current levels of around 4.75%, and the yield on the 10-year note will hit 4.50% or 4.675% from 4.16%. At higher levels, Michele expects to see big, institutional investors putting more money to work in high-quality bonds as concerns grow about the impact of a recession.

Michele urges caution, however, on parts of the bond market that are credit-sensitive, where issuers could start to run into problems making good on payments during a recession.

While many bond market observers are more sanguine about the outlook for credit-sensitive bonds, saying that corporate and consumer balance sheets are strong, Michele doesn’t buy that argument. “I’ve heard that rubbish before every recession, that it’s priced in, that the quality of borrowers is better,” he says. “Then the defaults start to hit, people worry about contagion, and the money starts pouring out of high yield.”

In particular, Holt expects a continued rough ride for technology stocks. Among many of the tech stocks that led the bull market higher, “they are in the maturation stage of their business models,” he says. Previously, even as the economy slowed, because companies would still be gaining market share, their stocks could remain buoyant.

Holt says investors should brace for a scenario broadly among technology companies similar to the experience following the dot-com bubble collapse. “Just like there was after 1999, you had maybe 75% of companies that didn’t make it, but there were those 25% that did.”

He also expects an earnings slowdown beyond tech stocks. “I think we will see a very tough Christmas, and retailers, which have already been hit, will continue to get hit,” Holt says. Even among energy stocks, which have buoyed the market in 2022 and helped keep third-quarter earnings in positive territory, growth will likely slow down next year, he says. “If energy prices flatten out, energy companies will be ok … but aren’t going to lift the market.”

Still, Holt sees the market favoring companies with strong cash flows. And as we head into the middle of 2023, as long as the Fed is able to stop raising interest rates, the focus will start to turn toward an economic rebound. At that point, cyclical stocks should come back into favor, including tech companies that have a strong advertising focus. Banks, too, should benefit as continued high interest rates will favor net interest margins on lending businesses, he says.

What’s Next for the Bond Market?

J.P. Morgan’s Michele says that in the Treasury market, the majority of the rise in yields—and decline in prices—is history. “If I think about where we started, we have probably had 80%-90% of the increase in Treasury yields we’re going to see.”

Still, Michele says the yield on the U.S. Treasury two-year note will rise to about 5.0% from its current levels of around 4.75%, and the yield on the 10-year note will hit 4.50% or 4.675% from 4.16%. At higher levels, Michele expects to see big, institutional investors putting more money to work in high-quality bonds as concerns grow about the impact of a recession.

Michele urges caution, however, on parts of the bond market that are credit-sensitive, where issuers could start to run into problems making good on payments during a recession.

While many bond market observers are more sanguine about the outlook for credit-sensitive bonds, saying that corporate and consumer balance sheets are strong, Michele doesn’t buy that argument. “I’ve heard that rubbish before every recession, that it’s priced in, that the quality of borrowers is better,” he says. “Then the defaults start to hit, people worry about contagion, and the money starts pouring out of high yield.”