Complacency Setting In

In a matter of weeks, the fate of 2022 for global equity markets moved from grim and uninspiring to okay but unsettling. The “Hope Phase” as coined by Goldman Sachs’ strategists seems to have already started. Meanwhile, the year has been difficult for both equity and bond investors. World equity markets lost 13% year to date, while bond markets declined 12%.

Instead of falling like a stone, financial markets have experienced several bear market rallies, with the latest one starting in early October.

Over the course of 2022, financial markets have had to digest higher for longer inflation rates, restrictive monetary policies, the war in Ukraine, growing fears of global recession and the worst financial conditions since 2020.

In the equity space, only a couple of sectors (energy, basic resources) and countries (Brazil) have recorded a positive performance so far this year.

Recently, a new narrative has taken the stage: Thanks to slowing inflation numbers, the work of the Fed should soon be over, with only two 50 bp hikes estimated to be left. With Fed fund rates close to the 5-5.5% range, the central bank is about to “pivot”, i.e. stop hiking during the first quarter of 2023.

This narrative has fueled a jump in equity multiples, helped by a better Q3 earnings season than most probably expected.

VIX futures dubbed the ‘fear indicator’ by some, are now around 20 after a yearly peak at 35 in early March. Yet the macro picture is deteriorating in many parts of the world, and the outlook for earnings remains that of a decline in the coming quarters. As The Economistrecently put it, this is the “strangest business cycle in living memory”.

A ‘Strange’ Cycle

The post-COVID world some expected might not be as clear-cut as it was only a year ago. Lockdowns are over in most of the world (except in China), but there are still issues in global supply chains. And climate change and hybrid work are changing consumer habits to some extent.

In the developed world, the rising cost of everything, fueled in part by the war in Ukraine, weighs on the purchasing power of both consumers and corporations. Yet, unemployment rates are relatively low in many countries and employees seem able to bargain for higher salaries. This will probably keep inflation higher for a bit longer than expected.

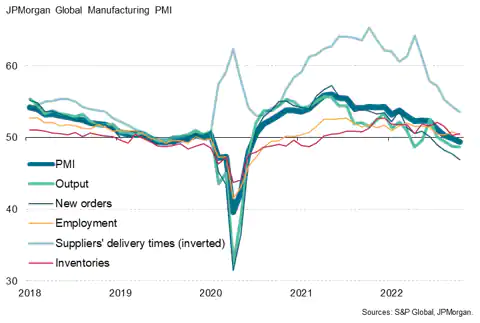

Even if households and corporations’ balance sheets are solid in most of the developed world, global economic growth is slowing down, as confirmed by the last Global Manufacturing PMI index (see chart) or the OECD leading indicator.

Source: S&P Global Market Intelligence, Nov 3, 2022.

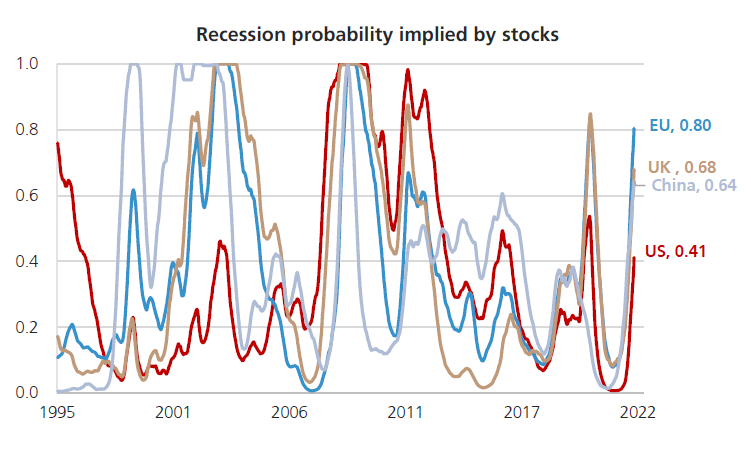

Advanced economic indicators are not the only ones flashing red. Yield curves in the US and euro are inverted over the course of the year, which also indicates a higher risk of recession.

Finally, several statistical models consider recession a more probable risk in several countries, starting with the euro area, due to the energy crisis, but also in China (where lockdowns are fueling social unrest) and in the United States (over the course of 2023).

Source: UBS, Nov 7, 2022.

Morningstar’s analyst Preston Caldwell estimates there is a 30-35% probability of a recession in the US next year, but that “any recession is likely to be short-lived”. In a nutshell, chances are inflation will probably slow down next year and growth will slow as well, with the risk of a global recession. The only question is: how severe will it be?

Fed Holds Most of the Cards

As usual for equity markets, most of what’s going to happen in 2023 will rely on the decisions of the U.S. Federal Reserve. The central bank has been slow to react to inflation but has since done a lot of catch-up. Markets are wondering if it has done enough, with 2 more 50 basis point rate hikes expected between now and early 2023. Yet there is a risk the Fed has only done the bare minimum so far and that its work is not over.

Some economists consider getting the Fed funds rates around 5% is enough to control inflation. Others are more cautious. “The Fed may be forced to push the economy into a deeper recession to curb inflation”, writes Savita Subramanian, US equity strategist at Bank of America Securities, in a recent report.

“Central banks can kill inflation, but it takes time for wage inflation to die”, wrote BCA Research analysts in a note date October 27, “If 2022 was the year that central banks’ monster tightening killed bond and stock market valuations, then 2023 will be the year that this monster tightening finally reaches the economy and kills profits and jobs”, they added.

The other issue for equity markets is that the U.S. Fed is also retiring liquidity, as shown by its balance sheet. When this happened in the past, it coincided with volatile markets and lower equity returns.

Source: Federal Reserve of St Louis, FRED database.

Earnings – Down, but by How Much?

In a typical recession, corporate earnings tend to decline by 20%, according to Bank of America. So far, the consensus still expects low single-digit growth in 2023, but some brokers (like Credit Suisse) anticipate a potential 15% contraction in 2023 if EPS were to return to their long-term trend (chart).

Faced with a slowing economy, corporations will have to deal with slowing or declining sales. Top-line growth should be helped by inflation, but lower volumes and higher cost inflation (through raw materials and wages) should weigh on margins.

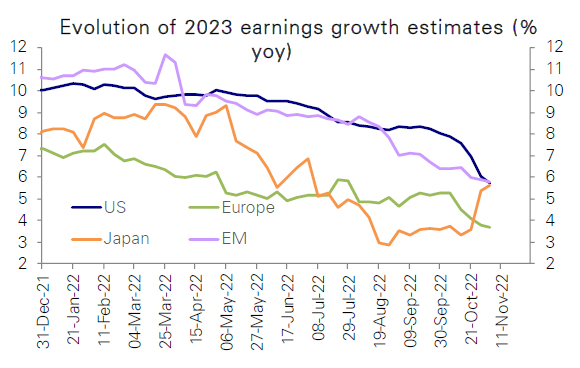

Higher cost of debt is also expected while taxes could also go higher, in particular in countries where fiscal pressure might intensify (China with its common prosperity program is an example). Consensus will continue cutting estimates for earnings over 2023, a trend that has already started (see chart).

Source: Deutsche Bank, Global Equity Strategy & Asset Allocation, Nov 4, 2022.

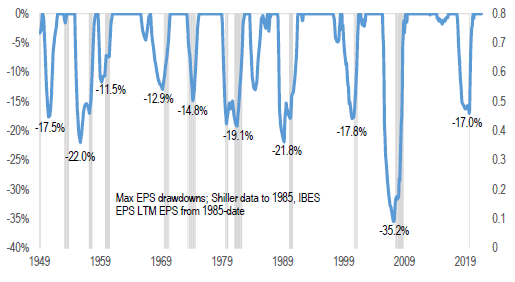

Earnings recessions don’t look the same, for obvious reasons. The underlying factors behind each recession vary over time – the last recession, in early 2020, was due to the COVID pandemic and the subsequent lockdowns.

If we look for historical precedents characterized by slowing growth and high inflation, we need to look at far back as the 70s. Based on the following chart from Credit Suisse, earnings at the time fell by 19%.

That’s how far the comparison can go since today’s structure and dynamics of the economy are quite different from the 70s.

Source: Credit Suisse, Nov 15, 2022.

Sectors don’t react the same way to recession either. In the US, Bank of America sees the biggest downside risk to Consumer Discretionary, where inflation should hit the most.

Technology might also be under pressure as years of solid top-line growth will be followed by more tepid growth. Goldman Sachs estimates mega-cap Tech stocks are forecast to grow by 8% in 2022, compared to 13% for the market.

Source: Credit Suisse, Nov 15, 2022.

Globally, “investors will increasingly shift their focus towards the earnings outlook, in particular, to how resilient corporate earnings are in the face of a sharp slowdown in economic activity coupled with inflationary pressure”, according to Julius Baer’s strategists.

In a recessionary world, quality and visibility on cash flows are probably characteristics investors will look for in their stock picking. Valuations will matter too.

Valuation Multiples Will Rebound Before EPS Hit a Trough

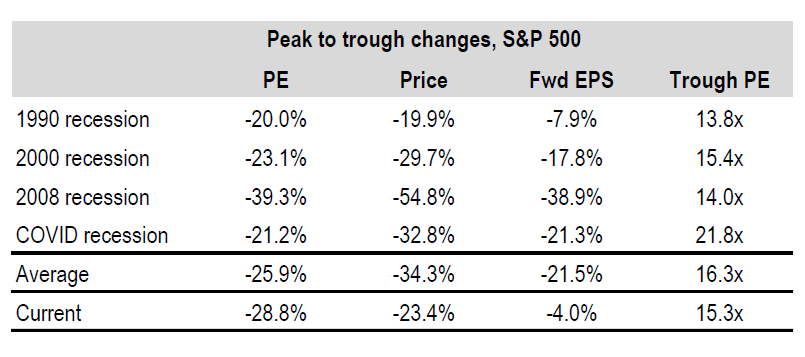

So far, in 2022, it appears the decline in the equity market has been largely driven by a de-rating in valuation multiples. In the US, the 12-month forward P/E of the S&P 500 has fallen from 21.5x at the end of 2021 to 17.5x, with a trough of 15.2x in late September, according to FactSet.

In the meantime, earnings estimates remained relatively stable, helped in part by the energy sector and the ability of some corporations to pass on more inflation to their clients than they had to bear with higher input costs.

For the coming year, there is a chance valuation multiples will remain in the driving seat. Yet with valuation multiples below their long-term average, equity investors already have a chance to start the year with a tailwind. According to Bank of America, US equity investors have an opportunity to invest and make a decent return over a 10-year time horizon: “The current normalized P/E of 22x implies 5.1%/yr annualized return over the next 10 years based on historical relationship”, they say.

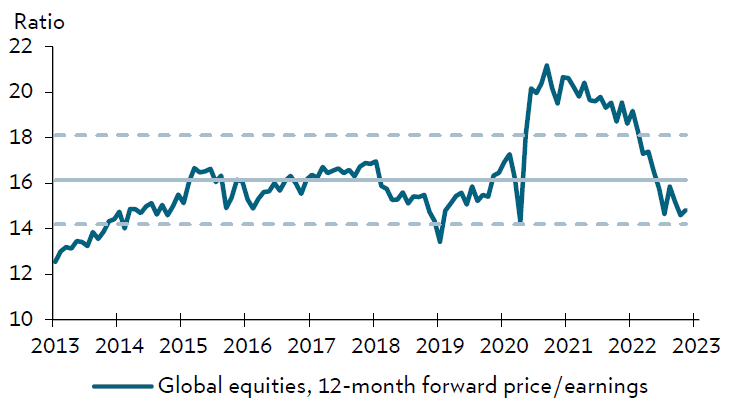

Outside the US, emerging and European equities are currently the most undervalued relative to the US.

Global equities indeed trade below their long-term average:

Source: Julius Baer, Nov 24, 2022

So far, the fall in valuation multiples shows the market is already discounting a decline in earnings in the coming months. The other driver of a market correction, i.e. higher equity risk premium (ERP), hasn’t moved yet.

If the market focus shifts from the Fed to the real economy and earnings, one could expect a decline in equity markets in the coming months. And if history is any guide, markets will probably rebound before the trough in earnings is reached, and before the recession is officially announced.

Conclusion

In trying to draw scenarios about where the market could go next year, we also must consider further upside/downside surprises for equity markets. Clearly, in the short run, a major downside is if inflation rates were to stay higher for longer, despite the decline in energy and food prices.

Another downside risk would be that the Fed stops its hiking cycle too early, and repeats the mistakes of the 70s, forcing it to restart rate hikes and confusing investors and the economy. The lack of liquidity in pockets of the markets could erode investor sentiment and bring about a rise in volatility (which has been pretty low recently).

So far, cracks in the financial markets have emerged outside the equity space (UK Gild, crypto) and have been contained by central banks, however, the war in Ukraine and the political tensions in China (both regarding COVID and its relationship with Taiwan) could also generate uncertainty and require a higher risk premium to own equities.

Upside risks for markets would be, in our opinion: theend of the war in Ukraine, the end of supply chain disruptions and a recession so short-lived it could be mistaken for a blip in the business cycle, making it less strange than currently anticipated.

Indeed, it’s a strange time to hold on to equities, and once again, valuation multiples will probably be a tailwind for equity portfolios, provided investors should have a long-term perspective in mind and keep their focus on the quality and earnings power of companies they want to add to their portfolios.