I grew up in Detroit, which had an outsize impact on my love of loud and fast cars. The days for those cars are waning, as the world moves toward a carbon transition. For all my love for these cars, I can’t ignore the rapid demand growth for (admittedly still speedy) electric vehicles that our equity analysts expect over the coming years. Yet such trends have helped give rise to the anti-ESG rhetoric that fills the headlines today, trying to restore the investing world to what it was before environmental, social, and governance considerations became important.

This raises the question: If ESG analysis and investing are so much trouble, is the topic important enough to keep focusing on? Couldn’t we just drop ESG altogether and get back to investing as we used to know it?

ESG Is Embedded in Our Lives

It’s not that simple. ESG issues are already embedded in our lives. Regulators and investors are increasingly focused on issues related to companies’ environmental and social actions, as evidenced by the SEC’s recommending new carbon disclosure requirements and sustainable-fund flows bucking the overall negative trend in 2022 (even with recent weakness). Meanwhile, consumers have increasingly voiced support for their own sustainability goals—even if their actions haven’t always matched their intentions.

Given this information, in order to generate the highest possible investment return, investors need to consider all financially material risks. That includes ESG and all other risks that could affect a company’s cash flows, no matter whether they align with their preferences. The coming boom in electric cars could lead to risks for some automakers, opportunities for others, and ramifications for companies up and down the supply chain. Regardless of my own preferences, it’s imperative that I take into account this environmentally related development and the impact it could have on my portfolio.

But investing is also a game of expectations—it’s not just about finding the best performers, but instead finding where valuation is mispriced or where the market hasn’t yet caught on to success stories. To that end, one sustainable-investing strategy could be to focus on finding companies that previously faced substantial ESG risk but have since drastically improved.

Finding ESG Stocks With Improving Ratings

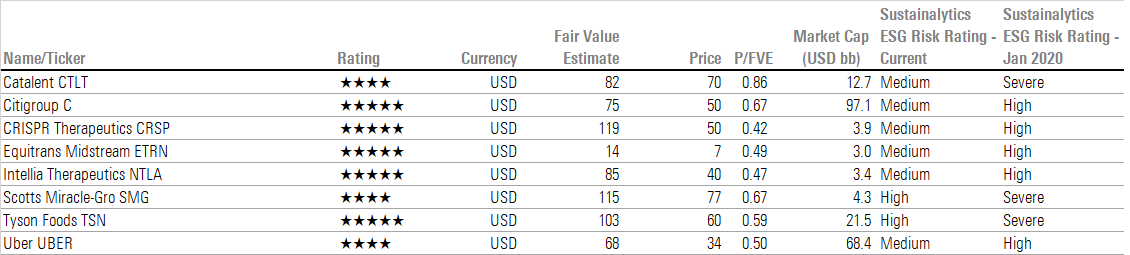

Below are eight such stocks of U.S. firms that were assigned Morningstar Sustainalytics ESG Risk Ratings of Severe or High in January 2020 but three years on have seen their ratings vastly improve. While these firms may have other near-term challenges that investors are focused on, the overall solid discount in current market prices versus their fair value estimates offers opportunities for long-term buyers. They include Catalent CTLT, Citigroup C, CRISPR Therapeutics CRSP, Equitrans Midstream ETRN, Intellia Therapeutics NTLA, Scotts Miracle-Gro SMG, Tyson Foods TSN, and Uber UBER.

ESG Is Only a Part of the Equation; High-Risk Stocks Can Still Offer Attractive Rewards

One investment strategy may be to focus on attractively priced ESG improvers. But we don’t recommend investing only in companies that face low ESG risk or that many consider sustainable.

Indeed, investors can use ESG information in many useful ways. For example, another strategy that also uses ESG information looks at stocks with a high degree of ESG risk and that still look cheap, on the theory that other investors may be overemphasizing these (among other) issues.

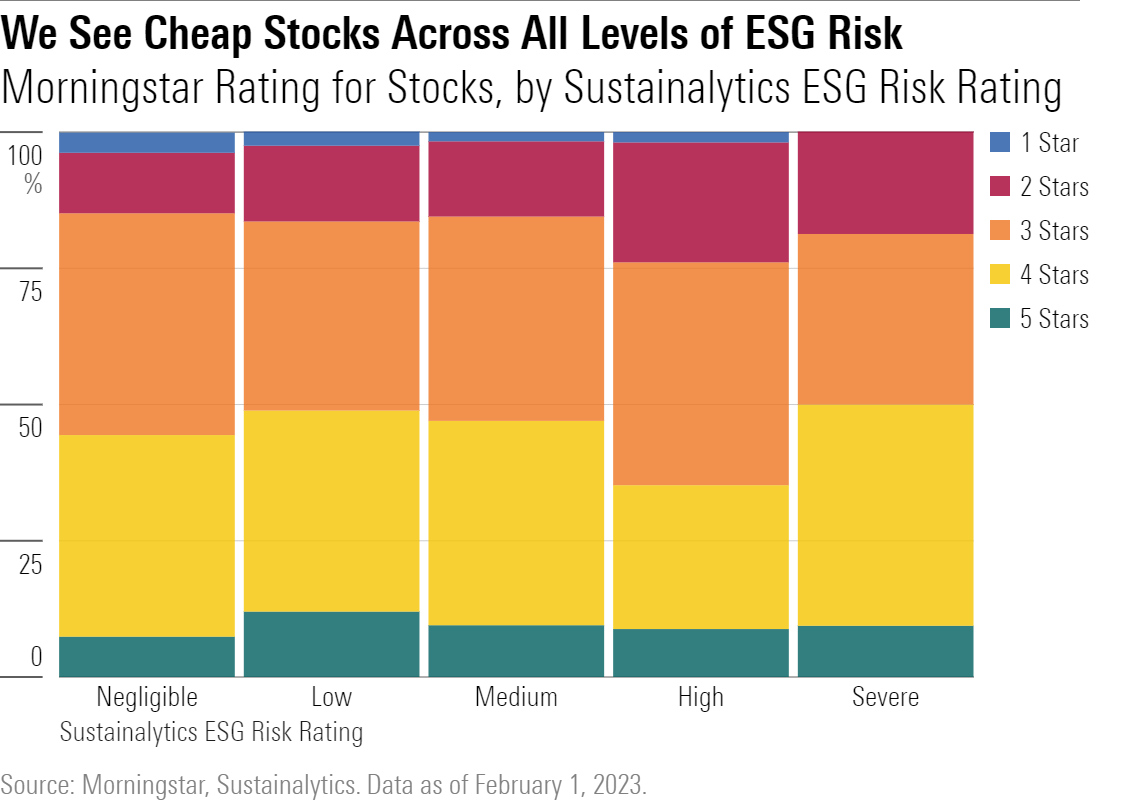

Our primary tool for determining whether these very risky stocks look sufficiently attractive is the Morningstar Rating for stocks, also known as the star rating. A stock with a 4- or 5-star rating suggests it’s substantially undervalued compared with our fair value estimate.

Among the companies we cover that have a High or Severe ESG Risk Rating, about 38% trade at either 4 or 5 stars. This is a bit lower than the 48% of our total coverage that has garnered these star ratings but nonetheless highlights that we can find plenty of cheap stocks among all levels of ESG risk.

In the end, profitable investing is about being properly rewarded for taking on risk. Aside from the improvers cited above, the three names below are worth taking a look at. Each faces lofty ESG risk, as evidenced by their High ESG Risk Ratings. But we think investors may be overly focused on these issues—each stock has carved an economic moat that should support sizable returns on invested capital despite ESG factors. Importantly, these names trade at substantial discounts to our estimates of fair value:

Boston Beer SAM

The slowing hard seltzer trend in the United States has plagued the craft brewer, with volume declining in 2022 through October. But the company’s beer portfolio continues to fare well, and Boston Beer’s solid brand equity has helped the firm hold pricing (and profit margins) in an uncertain and inflationary environment. While Morningstar Sustainalytics notes that weak management of water-resource issues has led to a High ESG Risk Rating, Boston Beer stock’s current price offers a sizable margin of safety versus our US$670 fair value estimate.

Meta Platforms META

Ongoing challenges for Meta stock from ESG issues like data privacy and security and business ethics lead to a High ESG Risk Rating, but the Facebook parent continues to perform strongly. In the recently reported fourth-quarter results, Meta’s network effect—which supports its wide Morningstar Economic Moat Rating—remained strong, with continued monthly user growth and even stronger engagement gains. We expect further improvement in ad conversions and cost reductions, supporting our forecast for the company to return to bottom-line growth, likely in the second half of 2023.

Wells Fargo WFC

This wide-moat bank has cast itself in a poor light over recent years, with significant business ethics issues related to a fake-accounts scandal that broke in late 2016. Morningstar Sustainalytics assigns the firm a High ESG Risk Rating. But despite Wells Fargo remaining in the middle of a multiyear rebuild, we’re already seeing glimpses of the transition to offense from defense, with the launch of multiple new card products and $2.2 billion of incremental internal investments expected in 2023. Continuing to meet expense goals and putting regulatory issues in the rearview will be key catalysts for the bank, but we view Wells Fargo stock as attractive.