Emerging markets arrived as an asset class when MSCI Emerging Market Index launched in 1988. In their infancy, they resembled today’s frontier markets rather than the current list of emerging markets with powerhouse global industries to their name. The original index started with 10 countries and failed to include many of what are now the largest emerging markets, such as China, Taiwan, and India.

By MSCI standards, the current list of developing countries sits at 24. According to IMF data, the gross domestic product of these 24 countries grew to $36.3 trillion in 2022 from $2.6 trillion in 1988. It’s easy to see why emerging markets captured the imagination of investors.

But market returns haven’t shared the same consistent growth pattern of their economies. The MSCI Emerging Markets Index nearly quintupled in its first six years. Then performance turned south, and it took another decade for the index to eclipse its previous high price from 1994. Then history repeated itself, with emerging markets shooting higher in the 2000s before flatlining over the past 12 years.

Given the prolonged performance swings and high risk involved, is investing in emerging markets worth the trouble?

Why You Should Invest in Emerging Markets

Emerging markets spin a powerful narrative. They grow fast and have plenty of runway left before they converge with developed markets. China and India each have higher populations than all developed countries combined. The potential for growth is astounding. Economic data supports the narrative. According to IMF data, the 24 countries making up the MSCI Emerging Market Index today combined to 13.4% of global nominal GDP in 1988. That number grew to 35.7% by the end of 2022. Over the past 10 years, emerging markets were responsible for 53.3% of the world’s nominal GDP growth.

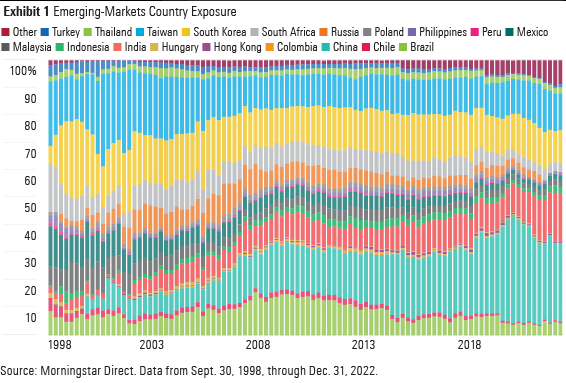

The emerging-markets portfolio reflects the changing landscape. China has grown into the dominant emerging-markets economy, now representing more than 28% of the Morningstar Emerging Markets Index. India has had a similar trajectory, starting at about 2% of the portfolio in 1998 and growing to over 17%. Countries like Mexico and South Africa have steadily lost ground to faster-growing countries.

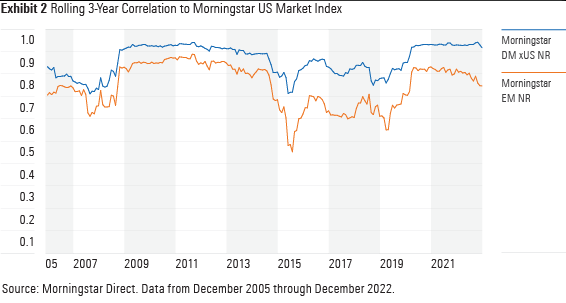

Emerging markets also tend to march to the beat of their own drum, at least more so than developed markets. This gives them an advantage as a diversifier for portfolios heavy in U.S. and other developed-markets stocks. Thanks to the lower correlation, emerging markets’ stand-alone volatility has a muted impact on a global portfolio.

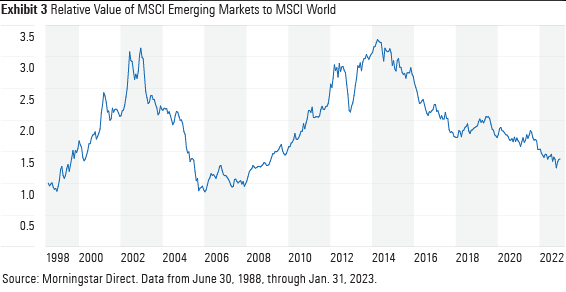

Another reason investors seek emerging-markets exposure is for its enthusiastic episodes of growth. Exhibit 3 demonstrates the massive swings of relative value between emerging and developed markets. Emerging markets’ returns exploded at the beginning of the 1990s and in the mid-2000s. But investors late to add emerging-markets stocks to their portfolios during these periods likely got the bull’s horns when outperformance shifted to prolonged periods of underperformance.

Why You Should Avoid Emerging Markets

It’s no surprise that emerging-markets stocks come with high risk. Since 1988, the standard deviation of the MSCI Emerging Markets Index was 7 percentage points higher than that of the MSCI World Index, which includes developed markets only. The impact on portfolio volatility by adding emerging-markets exposure is reduced by its relatively low correlation to developed markets. But it still adds an increment of risk and the potential for deeper drawdowns.

The biggest risks in markets are unforeseeable. Black swan events are extremely rare but can instantaneously change how we perceive decades of performance. Significant negative outcomes for investors are more common in emerging markets than developed ones. As a result, foreign governments play a large role in the success of emerging markets. Asset or company seizures and significant policy shifts are among the risks investors accept when they invest there.

Another risk is the market complexity inherent to emerging economies. Companies and fund managers must navigate varying legal systems, market structures, and instability. These complications reduce market efficiency and create risk for investors. In theory, taking on these risks should be rewarded with higher returns for investors. But that won’t always be the case.

Ways to Invest in Emerging Markets

The pros and cons of investing in emerging markets are clear. There’s no way of knowing what future risks or performance will look like. The next decade may see stellar performance reminiscent of the 2000s, or it may be a continuation of the long slog of underperformance from the 2010s. The only thing an investor gives up by excluding emerging markets is the potential for higher returns.

For those willing to accept the risks of investing in emerging markets, the next step is picking an exchange-traded fund. There are three main groups of emerging-markets ETFs: broad-market, rules-based active, and exclusionary.

Broad Market ETFs

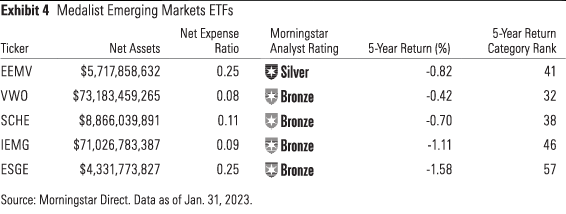

Exhibit 4 highlights the current Morningstar Medalist ETFs in the diversified emerging-markets Morningstar Category. Each of them comes with low fees and offers a diversified portfolio that won’t leave investors overexposed to the risks of any one company. Each has its own twist, but they are all good options for the long run. One differentiator is that FTSE indexes don’t consider South Korea an emerging market, whereas MSCI indexes do. As a result, the Schwab and Vanguard funds don’t hold South Korean stocks, but they make up between 7% and 13% of the portfolio for the medalist iShares ETFs, depending on the strategy.

Rules-Based Active ETFs

Complexity makes emerging markets less efficient than most market segments, so this category is one where active management may be the better option. Here, the active ETF market is dominated (in terms of assets) by systematic active strategies offered by Avantis and Dimensional Fund Advisors. These funds aren’t run by stock-pickers. They start with a broad market-cap-weighted portfolio of emerging-markets stocks and then strategically tilt toward companies with well-vetted characteristics proved to yield long-term outperformance. For example, they tend to target companies with strong value and quality factors. So far, the mutual fund versions of these strategies have yielded good results, and the ETFs follow identical strategies. But even the oldest of the ETFs, Avantis Emerging Markets Equity ETF AVEM, launched only in September 2019, so its track record is limited.

Exclusionary ETFs

The last cohort attempts to remove some of the greatest risks in emerging markets by limiting exposure to some of the most volatile countries and/or governments. Two U.S.-listed ETFs that fit the bill are WisdomTree Ex-State-Owned Enterprises Fund XSOE and the Freedom 100 Emerging Markets ETF FRDM. However, they address these risks in different ways. XSOE avoids government-owned and -influenced companies, which may be keener to serve political agendas than investor returns. FRDM only invests in countries that score highly on proprietary human and economic freedom scores, which tends to exclude volatile countries with heavy government influence.

In recent years, XSOE failed to circumvent government-driven drawdowns in emerging markets. It held 3.5% in Russian stocks—slightly less than the market—before Russia invaded Ukraine and the value of those holdings went to zero. It also had exposure to many of the Chinese tech stocks that crumbled under the pressure of Chinese government scrutiny in 2021. These events were a good reminder that government influence extends beyond direct ownership.

FRDM better navigated these challenges in emerging markets by not owning any stocks in Russia or China. FRDM is appealing from a political risk perspective. But much of the draw to emerging markets stems from the growth potential of China and similar countries. While FRDM was a top performer in its category since inception, it’s unclear how it will perform when emerging markets rally.

Maintaining Emerging-Markets Exposure

Investors should feel at peace with their decision whether they allocate to emerging markets or not. There’s no clear right answer. Regardless of what investors choose, they should stick with their decision. Chasing performance can yield brutal results in these markets. And emerging markets can go for years without a substantial rally. Patience is a virtue when investing in emerging markets.