A new taxation year is only days away, bringing with it some inflation-related adjustments to tax brackets, credit amounts and benefits. The Canada Revenue Agency has indexed these amounts for 2024 at 4.7% over last year’s levels. That rate is based on the average Consumer Price Index during the 12 months ended Sept. 30, 2023, compared to the same period a year earlier.

Here are some new numbers and key dates to consider for 2024, starting with tax brackets on employment income:

1: 15% on the first $55,868 of employment and “other income” (compared with the first $53,359 in 2023)

2: 20.5% on $55,868 to $111,733 (versus $53,360 to $106,717)

3: 26% on $111,734 to $173,205 ($106,7187-$165,430)

4: 29.3% on $173,206 to $246,752 ($165,431-$235,675)

5: 33% on the amount over $246,752 ($235,752)

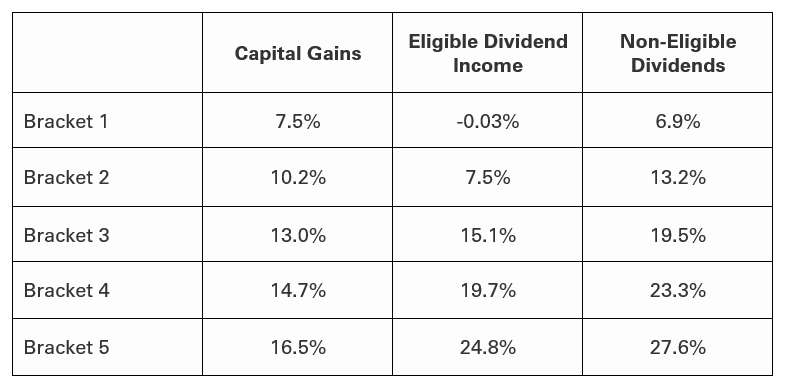

The respective rates for capital gains (based on one-half of gains being subject to tax), eligible dividend income (generally applicable to large Canadian corporations’ dividends) and non-eligible dividends (those paid out by smaller Canadian corporations) in each federal bracket for 2024 are as follows:

New Tax Brackets for Investments in 2024:

Combined Federal and Provincial Tax Rates

Individual provinces also have adjusted their brackets accordingly for 2024. Here is an overview of how this affects combined federal and provincial tax rates for employment and other income in the four biggest provinces:

- Ontario’s lowest combined federal and provincial bracket now applies to those with taxable income of $51,446 or less, compared with $49,231 in 2023, and this tranche of income continues to be taxed at 20%. The top bracket now applies to those with taxable income over $246,752, versus $235,675 last year, and is taxed at 53.5%. An individual with a taxable income of $100,000 continues to pay no more than 31.5% in taxes.

- In Quebec, the lowest combined federal/provincial bracket is now capped at $51,780 versus $49,275 in 2023 and is taxed at 26.5% (unchanged). The top bracket applies to amounts above $246,752, an increase from $235,675 last year, and is taxed at 53.3% (no change). An individual with a taxable income of $100,000 continues to pay no more than 31.5% in taxes.

- British Columbia’s lowest combined federal/provincial bracket now reaches $47,937, up from $45,654 last year and continues to be taxed at 20%. Its top bracket applies to taxable income above $252,752, versus $240,716 in 2023, and is taxed at 53.5%. A $100,000 earner pays a maximum tax of 31%.

- Alberta now has a bottom combined federal/provincial tax bracket ceiling of $55,867, up from $53,369 last year, and continues to be taxed at 25%. Its top bracket continues to be taxed at 48% and applies to income above $355,845, up from $341,502 in 2023. A $100,000 individual’s top tax rate is 30.5%.

Canadian Tax Credits in 2024

Here is a summary of changes to key federal non-refundable tax credits for 2024:

Basic Personal Amount: $15,705 (up from $15,000 in 2023). No tax is payable on taxable income up to this level.

Age: $8,790 ($8,396). This credit is available to those age 65 and over and is gradually “clawed back” for those who reported net income in 2021 of approximately $44,300 to $103,000 when the credit is eliminated.

Disability: $9,872 ($9,428)

Pension income: $2,000 (unchanged)

Medical expenses: $2,759 ($2,635) and continues to be capped at 3% of net income.

For provincial tax purposes, these credits also have been similarly increased. For example, in Ontario, the basic personal amount applicable to provincial tax is now $12,399, up from $11,865 in 2023. In Quebec, the amount is now $18,056, versus $17,183.

Contribution Limits

- RRSP Dollar Limit: The 2024 limit is $31,560 (i.e., for contributions made by March 1, 2025), up from $30,780 for 2023 (March 1, 2024, deadline). This annual limit cannot exceed 18% of your previous taxation year’s earned income. The actual maximum contribution in any given year is determined by your total contribution room generated by unused contributions over the years.

- TFSA Limit: $7,000, up from $6,500 in 2023. For those who have never contributed to a TFSA, the cumulative limit is now $95,000.

- OAS Clawback Range: Old Age Security income is clawed back for higher-income recipients, under the CRA’s “monthly recovery tax.” If your 2023 net income was $86,912 or higher, part or all of the OAS you received during that year must be repaid during the July 2024-June 2025 period. For those aged 65-74, OAS income will be completely taxed back if your net income was $142,609 or higher ($148,179 for those age 75 and older). For OAS received during 2024, the clawback threshold is estimated to be about $91,000.

- CPP Contributions: Premiums payable to the Canada Pension Plan (and the Quebec Pension Plan) is 5.95% of an employee’s earnings, unchanged from 2023, while the premium amount for self-employed individuals remains 11.9%. The maximum annual contribution for employees (and their employers) is now $3,867, compared with $3754 in 2023. For self-employed individuals, the maximum is $7735, up from $7509. The yearly maximum pensionable earnings (YMPE) is now $68,500, up from $66,600 last year. For 2024, an additional premium will be applied for those with earnings above the YMPE, up to an additional maximum pensionable earnings level of $73,200, for a maximum additional contribution of $188 ($376 for self-employed). The additional-YMPE limit for 2025 is estimated to be $79,400.

- EI Contributions: The maximum Employment Insurance contribution for an individual has risen to $1049, up from $1002 in 2023. The maximum annual insurable earnings is now $63,200, up from $61,500 last year.

Your 2024 Canadian Tax Calendar

Personal income tax deadlines:

- 2023 RRSP contribution: March 1, 2024 (The 2024 RRSP contribution deadline is March 1, 2025)

- Quarterly installments for 2024 income tax (if applicable, i.e., tax not deducted at source): March 15, June 15, September 15, December 15

- T4 employment-income slips to be sent out: end of February

- T5s: end of February

- T3s: end of March

- Income tax return filing for individuals: April 30

- Income tax return filing for self-employed individuals: June 17 (the normal deadline of June 15 falls on a Saturday this year)

- Payment of taxes owed (including for self-employed): April 30

- Deceased taxpayers: If a death occurred during 2023 between January and end of October, the deadline to file return in respect of the year of death is April 30. For a death that occurred during November or December 2023, the deadline is six months following the date of death. Any outstanding amount of tax for the deceased are due on the above return-filing dates.

- Collapse RRSP: If you turn 71 this year (i.e., during 2024) your RRSP must be converted to a registered retirement income fund or a life annuity by Dec. 31, 2024 (but realistically this should be arranged earlier in December).

Sales Tax Deadlines

(The following applies to self-employed individuals who file H/G/QST return annually.)

- Quarterly installment dates for 2022 H/G/QST remittances: one month after the end of the period

- Deadline to file H/G/QST return: June 17 (as June 15 falls on a Saturday)

- Deadline for paying H/G/QST owing in excess of amounts paid by installment: April 30

:quality(80)/cloudfront-us-east-1.images.arcpublishing.com/morningstar/EC7LK4HAG4BRKAYRRDWZ2NF3TY.jpg)