:quality(80)/cloudfront-us-east-1.images.arcpublishing.com/morningstar/MQJKJ522P5CVPNC75GULVF7UCE.jpg)

Palantir Technologies PLTR is set to release its first-quarter earnings report on May 6. Here’s Morningstar’s take on what to look for in Palantir’s earnings and stock.

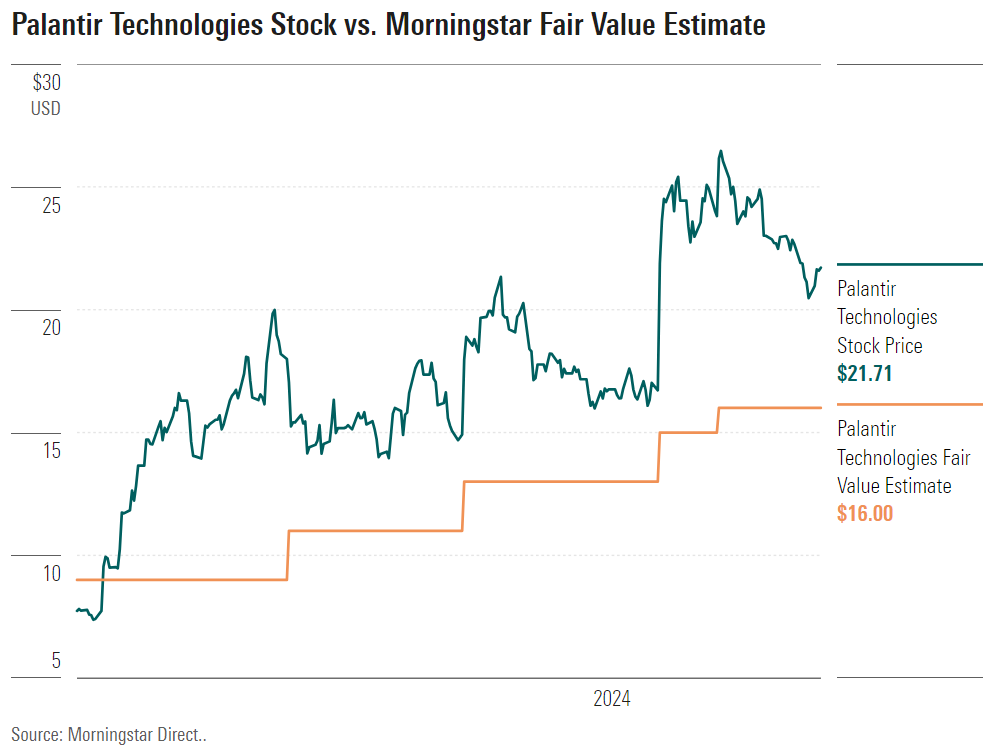

Key Morningstar Metrics for Palantir

Fair Value Estimate: US$16.00

Morningstar Rating: 2 stars

Morningstar Economic Moat Rating: Narrow

Morningstar Uncertainty Rating: Very High

Earnings Release Date

- Monday, May 6, after the close of trading

What to Watch for In Palantir’s Q1 Earnings

- Billings: To get a better sense of Palantir’s success with artificial intelligence and whether its boot camps (hands-on training sessions for customers to implement the Artificial Intelligence Platform into their business) are leading to customer conversions, investors will be keenly seeking forward-looking indicators of demand for the firm’s solutions.

- Customer additions (particularly in commercial): Just like last quarter, we will keep a keen eye on whether new customers are onboarding Palantir’s platforms, and to what degree the Artificial Intelligence Platform is helping it land users. Again, we will be curious about whether the firm’s tremendous number of boot camps will translate into actual customers.

- Government sales: In the wake of the firm scoring the TITAN contract with the U.S. government, management’s commentary on this vertical will be of interest. We would expect an uptick not only due to the contract but also a general uplift in governmental spending on AI, big data, etc.

Fair Value Estimate for Palantir

With its 2-star rating, we believe Palantir’s stock is overvalued compared with our long-term fair value estimate of US$16 per share, which implies a 2024 enterprise value/sales multiple of 12 times. We forecast Palantir’s revenue to grow at a 21% compound annual growth rate over the next five years as the firm expands both governmental and commercial operations.

We expect the majority of this top-line growth to be driven by commercial clients as the firm seeks to broaden its commercial client base. While government clients can be sticky, large governmental contracts create lumpiness in revenue. As a result, Palantir’s shift to more commercial clients should create a more ratable revenue mix. We also expect the firm to continue expanding sales within its existing client base. We view Palantir’s strong net retention rate as an indicator of this.

Economic Moat Rating

We assign Palantir a narrow moat owing primarily to strong switching costs associated with its platforms and secondarily to intangible assets in the form of strong customer relationships the firm has built up over the years.

We think Palantir’s two main platforms, Gotham and Foundry, both benefit from high customer switching costs, as evidenced by its gross and net retention metrics. Palantir has exhibited strong customer growth while diversifying its business away from lumpy governmental contracts toward commercial clients. As a result, although we forecast a couple of more years of hefty operating losses, we expect the firm to generate excess returns over invested capital over the next decade.

We think Foundry and Gotham present switching costs, as evidenced by the firm’s high retention rates. Across our coverage, we see that spending by large organizations tends to be sticky. Palantir’s clients, especially governments, are using its products for incredibly important cases in which errors can be potentially catastrophic or fatal. Further, we see Palantir moving its clients along the upselling schedule by either analyzing more data or offering them additional capabilities. In either case, we see Palantir expanding its touch points across a client’s organization, making churn less likely over time.

Financial Strength

We view Palantir’s financial position as healthy. The company ended fiscal 2023 with around US$3.7 billion in cash and liquid investments and no debt. While Palantir only posted GAAP profitability in 2023, we expect the firm to continue this trend while generating strong cash flow margins as it increases its operating leverage by toning down some of its research and sales expenditures.

Risk and Uncertainty

We assign Palantir a Very High Uncertainty Rating due to some key risks that we view as potentially impeding its growth trajectory. While the firm has landed high-value commercial and government clients over the years, we have found the executive team’s execution to be questionable at best. The firm’s sales strategy has led to relatively poor customer acquisition, despite it being in the commercial space for many years, Palantir’s commercial customer count is only slightly more than 200. While the firm has pivoted to a module-based sales model that should bolster commercial customer additions, the execution of this strategy remains to be seen.

PLTR Bulls Say

- Palantir has strong secular tailwinds, as the AI/ML market is expected to grow rapidly due to the exponential increase in data harvested by organizations.

- With products targeting both commercial and governmental clients, Palantir has a distributed top line, with noncyclical governmental revenue insulating the overall top line during lean times.

- Palantir’s focus on modular sales could lead to substantially more commercial clients, which it could subsequently upsell.

PLTR Bears Say

- By not selling to countries or companies that are antithetical to its mission and cultural values, Palantir has self-restricted its growth opportunities.

- Palantir’s AI platform is off to a good start, but we anticipate robust competition in the years ahead.

- Palantir’s executive team has made questionable strategic decisions in the past. While past performance isn’t necessarily indicative of future results, the missteps could merit caution.

This article was compiled by Sokhoeun Noeut.

The author or authors do not own shares in any securities mentioned in this article.